Weekly Market Update | Week 36

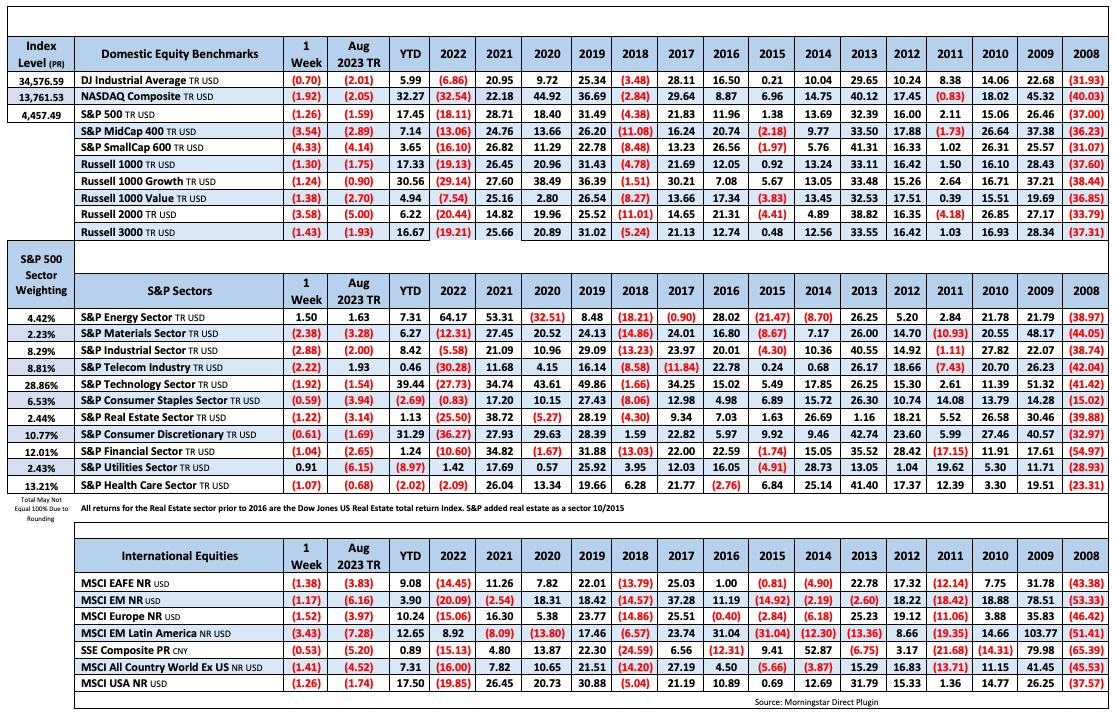

US equities were down this week, with the S&P and Nasdaq dropping back below their 50-day moving averages. Big tech was mostly higher this week but AAPL (6.0%) was a big drag amid a Chinese ban on iPhone use at government agencies and worries about premium-model pricing power ahead of the company’s 12-Sep product event. NVDA (6.1%) was another notable decliner. Other laggards included airlines (some fuel-cost warnings), tech hardware, semis, banks (particularly regionals amid some renewed CRE worries), industrial metals, machinery, homebuilders, and China tech. Outperformers included managed care, software, exchanges, refiners, and utilities.

Treasuries were weaker overall, though yields moderated from mid-week highs (the 2Y rose back above 5% on Wednesday). There was a lot of focus on continued strength in the economic data, particularly the better-than-expected August ISM Services report, as well as high corporate issuance. The dollar was stronger again, with the DXY +0.8% posting its eighth straight weekly gain and hitting its highest level since March. Gold was lower, dropping 1.2% after two weekly gains. Oil rose again, with WTI +2.3% hitting its highest level since November 2022 after Saudi Arabia and Russia announced a longer-than-expected extension of their voluntary output cuts.

It was a generally risk-off week in the market. A major factor was traction in the “good news is bad news” dynamic, with continued strong economic data raising questions about the Fed’s rate policy going forward. In an otherwise light economic week, there was a big focus on a stronger-than-expected read for August ISM Services, which showed notable monthly gains in new orders and employment alongside an uptick in prices paid. The week also saw initial jobless claims hit their lowest mark since February in another sign of labor-market strength. Friday also saw a slight increase for the August Manheim used vehicle index, which had declined in each of the previous four months. These factors, alongside with a notable surge in corporate debt issuance, helped push Treasury yields higher and roll back some of the prior week’s yield decline at the short end of the curve. All that said, there was not a lot of movement in market-based expectations for the Fed’s rate trajectory, which remained firm for a pause at this month’s FOMC meeting and generally pointing to no further hike this year. You can check out the expectations on the CME FedWatch Tool.

Several other factors also weighed on equities this week. Oil strength driven by Russian and Saudi production-cut announcements (and looking past recent concerns about the resilience of China demand) raised the specter of further inflationary pressures. There were some cautious details in Fed’s latest Beige Book report, including notes about slowing retail spending ex autos, higher delinquencies on consumer credit lines, and thoughts that spenders may have exhausted pandemic savings. Continued strength in the dollar played into the narrative of tighter financial conditions. And the high-profile sparring between major automakers and the United Auto Workers union ahead of next week’s contract deadline clouded the market’s mood.

Nevertheless, multiple analysts continue to expect the market to trade in a fairly narrow range at least through year-end, with some offsets seen to the bearish case. Economic strength also plays into the soft-landing thesis (even as outlined by multiple Fed speakers). Expectations remain that the Fed is at its rate ceiling for the cycle. Forecasters continue to see some disinflationary factors at work, with WMT’s news on pay changes this week a possible sign of the labor market coming back into balance. KR +2.1% also said Friday that disinflation has been occurring at a greater rate than originally anticipated. Finally, seasonal concerns about a September slump continue to be generally waved off.

The critical event next week will be the 9/13 release of the August CPI report, which is expected to see an uptick in the headline driven by energy prices but a third-straight monthly drop in core prices. The week will also see the NY Fed’s latest Survey of Consumer Expectations (9/11),August PPI and retail sales reports (9/14) and the preliminary September consumer sentiment report, including inflation expectations (Friday 9/15). Fedspeak will be absent with the Fed in its blackout period ahead of the 19-20 FOMC meeting.

Fixed Income

Yield Curve

July FOMC Statement July Fed Minutes Balance Sheet Reduction Plan Credit, Liquidity and Balance Sheet Federal Reserve Dot Plots

Treasury.gov yields FOMC Policy Normalization Statement Longer- Run Goals Jan 2022

Foreign Exchange Market

Energy Complex

The Baker Hughes rig count was up 1 this week. There are 632 oil and gas rigs operating in the US – Down 127 from last year.

Metals Complex

Employment Picture

Weekly Unemployment Claims – Released Thursday 9/7/2023 –In the week ending September 2, the advance figure for seasonally adjusted initial claims was 216,000 decreasing 13,000 from the previous week’s revised level. The 4-week moving average was 229,250 a decrease of 8,500 from the previous week’s revised average.

August Jobs Report – BLS Summary – Released 9/1/2023 – The US Economy added 187k nonfarm jobs in August and the Unemployment rate edged up to 3.8%. Average hourly earnings increased 8 cents to $33.82. Hiring highlights include +102k Education and Health Services, +40k Leisure and Hospitality, and +22k Construction.

- Average hourly earnings increased 8 cents/0.2% to $33.82.

- U3 unemployment rate increased 0.3% to 3.8%. U6 unemployment rate increased 0.4% to 7.1%.

- The labor force participation rate increased by 0.2% to 62.8%.

- Average work week increased 0.1 hours to 34.4 hours.

Job Openings & Labor Turnover Survey JOLTS – Released 8/29/2023 – The number of job openings decreased to 8.8 million on the last business day of July, the U.S. Bureau of Labor Statistics reported. Over the month the number of hires and total separations were little changed at 5.8 million and 5.5 million, respectively. Within separations, quits (3.5 million) decreased and discharges (1.6 million) changed little.

Employment Cost Index – Released 7/28/2023 – Compensation costs for civilian workers increased 1.0% for the 3-month period ending in June 2023. The 12-month period ending in June 2023 saw compensation costs increase by 4.5. The 12-month period ending June 2022 increased 5.1%. Wages and salaries increased 4.6 percent over the 12-month June 2023 and increased 5.3 percent for the 12-month period ending in June 2022. Benefit costs increased 4.2 percent over the 12-month period ending June 2023 and increased 4.8 percent for the 12-month period ending in June 2022. This report is published quarterly.

This Week’s Economic Data

Links take you to the data source

Consumer Credit – Released 9/8/2023 – Consumer credit increased at a seasonally adjusted annual rate of 2.5 percent in July. Revolving credit increased at an annual rate of 9.2 percent, while nonrevolving credit increased at an annual rate of 0.2 percent.

U.S. Trade Balance – Released 9/6/2023 – The U.S. Census Bureau and the U.S. Bureau of Economic Analysis announced that the goods and services deficit was $65.0 billion in July, up $1.3 billion from $63.7 billion in June. June exports were $251.7 billion, $3.9 billion more than June exports. July imports were $316.7 billion, $5.2 billion more than June imports. The July increase in the goods and services deficit reflected an increase in the goods deficit of $2.0 billion to $90.0 billion and an increase in the services surplus of $0.7 billion to $25.0 billion.

PMI Non-Manufacturing Index – Released 9/5/2023 – Economic activity in the services sector expanded in August for the eighth consecutive month as the Services PMI® registered 54.5 percent, 1.8 percentage point higher than July’s reading of 52.7 percent.

Recent Economic Data

Links take you to the data source

U.S. Construction Spending– Released 9/1/2023 – Construction spending during July 2023 was estimated at a seasonally adjusted annual rate of $1,972.6 billion, 0.7 percent above the revised June estimate of $1,958.9 billion. The July figure is 5.5 percent above the July 2022 estimate of $1,869.3 billion.

PMI Manufacturing Index – Released 9/1/2023 – The August Manufacturing PMI registered 47.6 percent, 1.2 percentage points higher than the 46.4 percent recorded in July. Regarding the overall economy, this figure indicates a ninth month of contraction after a 30-month period of expansion. The New Orders Index remained in contraction territory at 46.8 percent, 0.5 percentage points lower than the figure of 47.3 percent recorded in July. The Production Index reading of 50.0 percent is a 1.7-percentage point increase compared to July’s figure of 48.3 percent.

US Light Vehicle Sales– Released 8/31/2023 – U.S. light vehicle sales were at a seasonally adjusted annual rate (SAAR) of 15.732 million units in August.

Chicago PMI – Released 8/31/2023 – Chicago PMI remained in contraction territory in August increasing to 48.7 points up from 42.8 points in August. This increase surpassed expectations but still marks twelve months in contractionary territory.

Personal Income – Released 8/31/2023 – Personal income increased $45.0 billion (0.2 percent at a monthly rate) in July. Disposable personal income (DPI) increased $7.3 billion (0.1 percent). Personal consumption expenditures (PCE) increased $144.6 billion (0.8 percent).

Second Estimate of 2nd Quarter 2023 GDP – Released 8/30/2023 – Real gross domestic product (GDP) increased at an annual rate of 2.1 percent in the second quarter of 2023, according to the “second” estimate released by the Bureau of Economic Analysis. The GDP estimate released today is based on more complete source data than were available for the “advance” estimate issued last month which had GDP increasing at 2.4 percent. In the first quarter, real GDP increased 2.0 percent. The increase in real GDP reflected increases in consumer spending, nonresidential fixed investment, state and local government spending, private inventory investment, and federal government spending that were partly offset by decreases in exports and residential fixed investment. Imports, which are a subtraction in the calculation of GDP, decreased.The updated estimates primarily reflected downward revisions to private inventory investment and nonresidential fixed investment that were partly offset by an upward revision to state and local government spending.

Consumer Confidence– Released 8/29/2023 – Consumer Confidence decreased in August to 106.1, down from 114.0 in July. August’s decline reflected dips in both the current conditions and expectations indexes. Consumers were once again preoccupied with rising prices in general, and for groceries and gasoline in particular.

Durable Goods Released 8/24/2023 – New orders for manufactured durable goods in July, down following four consecutive months of increases, decreased $15.5 billion or 5.2 percent to $285.9 billion, the U.S. Census Bureau announced today. This followed a 4.4 percent June increase. Excluding transportation, new orders increased 0.5 percent. Excluding defense, new orders decreased 5.4 percent. Transportation equipment, also down following four consecutive months of increases, drove the decrease, $16.4 billion or 14.3 percent to $98.7 billion.

New Residential Sales Released 8/23/2023 – Sales of new single‐family houses in July 2023 were at a seasonally adjusted annual rate of 714,000, according to estimates released jointly by the U.S. Census Bureau and the Department of Housing and Urban Development. This is 4.4 percent above the revised June rate of 684,000 and is 31.5 percent above the July 2022 estimate of 543,000. The median sales price of new houses sold in July 2023 was $436,700. The average sales price was $513,000. At the end of July, the seasonally adjusted estimate of new homes for sale was 437,000, a supply of 7.3 months at the current sales rate.

Existing Home Sales Released 8/22/2023 – July 2023 brought 4.07 million in sales, a decrease of 2.2% from June. The median sales price was $406,700. The current unsold housing inventory was 3.3 months of inventory.

Housing Starts– Released 8/16/2023 – July housing starts came in at 1,452,000, 3.9% above the June estimate and 5.9% above the July 2022 rate. Building permits were 0.1% above the June rate at $1,441,000 and 13.0% below the July 2022 rate.

Industrial Production and Capacity Utilization Released 8/16/2023 – Industrial production increased 1.0% in July following two months of decline. Utilities output increased 5.4%. Manufacturing increased 0.5%. Mining increased 0.5%. Capacity utilization increased to 79.3% in July, 0.4% below the long-run average.

Retail Sales– Released 8/15/2023 – Headline retail sales increased 0.7% in July and are up 3.2% above July 2022.

Producer Price Index – Released 8/11/2023 – The Producer Price Index for final demand increased 0.3 percent in July, seasonally adjusted. Final demand were unchanged in June and decreased 0.3 in May. On an unadjusted basis, the index for final demand moved up 0.8 percent for the 12 months ended in July.

Consumer Price Index – Released 8/10/2023 – The Consumer Price Index for All Urban Consumers rose 0.2 percent in July on a seasonally adjusted basis, after increasing 0.2 percent in June. Over the last 12 months, the all items index increased 3.2 percent before seasonal adjustment.

Next week we get data on CPI, PPI, Retail Sales, Industrial Production and Capacity Utilization.

Data Sources:

Bureau of Economic Analysis (BEA)

Congressional Budget Office (CBO)

U.S. Bureau of Labor Statistics (BLS)

Federal Reserve Economic Data (FRED Charts)

CME Fed Watch

U.S. Treasury – Yields

U.S. Census Bureau

Institute for Supply Management (ISM)

Weekly DOL Employment Data

BLS Monthly Jobs Report

JOLTS

US Energy Admin (EIA)

BLS Consumer Price Index CPI

BLS Producer Price Index PPI

Atlanta Fed GDPNOW

NY Fed Nowcast GDP

US Census Bureau Housing Starts

Consumer Credit

USCB Retail Sales

Construction Spending

Federal Reserve Dot Plots

NY Empire Index

Philadelphia Federal Reserve

P/E Ratio Data -Yardeni Research

Technical Analysis Info:

StockCharts.com – Financial Charts

Exponential vs Simple moving average

Koyfin.com

Other Links:

1973 Arab Oil Embargo

Hunt Brothers Silver

Long-Term Capital bailout

Asian Contagion

Week 36 Talking Points

Table of Contents

Weekly Market Update | Week 36

US equities were down this week, with the S&P and Nasdaq dropping back below their 50-day moving averages. Big tech was mostly higher this week but AAPL (6.0%) was a big drag amid a Chinese ban on iPhone use at government agencies and worries about premium-model pricing power ahead of the company’s 12-Sep product event. NVDA (6.1%) was another notable decliner. Other laggards included airlines (some fuel-cost warnings), tech hardware, semis, banks (particularly regionals amid some renewed CRE worries), industrial metals, machinery, homebuilders, and China tech. Outperformers included managed care, software, exchanges, refiners, and utilities.

Treasuries were weaker overall, though yields moderated from mid-week highs (the 2Y rose back above 5% on Wednesday). There was a lot of focus on continued strength in the economic data, particularly the better-than-expected August ISM Services report, as well as high corporate issuance. The dollar was stronger again, with the DXY +0.8% posting its eighth straight weekly gain and hitting its highest level since March. Gold was lower, dropping 1.2% after two weekly gains. Oil rose again, with WTI +2.3% hitting its highest level since November 2022 after Saudi Arabia and Russia announced a longer-than-expected extension of their voluntary output cuts.

It was a generally risk-off week in the market. A major factor was traction in the “good news is bad news” dynamic, with continued strong economic data raising questions about the Fed’s rate policy going forward. In an otherwise light economic week, there was a big focus on a stronger-than-expected read for August ISM Services, which showed notable monthly gains in new orders and employment alongside an uptick in prices paid. The week also saw initial jobless claims hit their lowest mark since February in another sign of labor-market strength. Friday also saw a slight increase for the August Manheim used vehicle index, which had declined in each of the previous four months. These factors, alongside with a notable surge in corporate debt issuance, helped push Treasury yields higher and roll back some of the prior week’s yield decline at the short end of the curve. All that said, there was not a lot of movement in market-based expectations for the Fed’s rate trajectory, which remained firm for a pause at this month’s FOMC meeting and generally pointing to no further hike this year. You can check out the expectations on the CME FedWatch Tool.

Several other factors also weighed on equities this week. Oil strength driven by Russian and Saudi production-cut announcements (and looking past recent concerns about the resilience of China demand) raised the specter of further inflationary pressures. There were some cautious details in Fed’s latest Beige Book report, including notes about slowing retail spending ex autos, higher delinquencies on consumer credit lines, and thoughts that spenders may have exhausted pandemic savings. Continued strength in the dollar played into the narrative of tighter financial conditions. And the high-profile sparring between major automakers and the United Auto Workers union ahead of next week’s contract deadline clouded the market’s mood.

Nevertheless, multiple analysts continue to expect the market to trade in a fairly narrow range at least through year-end, with some offsets seen to the bearish case. Economic strength also plays into the soft-landing thesis (even as outlined by multiple Fed speakers). Expectations remain that the Fed is at its rate ceiling for the cycle. Forecasters continue to see some disinflationary factors at work, with WMT’s news on pay changes this week a possible sign of the labor market coming back into balance. KR +2.1% also said Friday that disinflation has been occurring at a greater rate than originally anticipated. Finally, seasonal concerns about a September slump continue to be generally waved off.

The critical event next week will be the 9/13 release of the August CPI report, which is expected to see an uptick in the headline driven by energy prices but a third-straight monthly drop in core prices. The week will also see the NY Fed’s latest Survey of Consumer Expectations (9/11),August PPI and retail sales reports (9/14) and the preliminary September consumer sentiment report, including inflation expectations (Friday 9/15). Fedspeak will be absent with the Fed in its blackout period ahead of the 19-20 FOMC meeting.

Fixed Income

Yield Curve

July FOMC Statement July Fed Minutes Balance Sheet Reduction Plan Credit, Liquidity and Balance Sheet Federal Reserve Dot Plots

Treasury.gov yields FOMC Policy Normalization Statement Longer- Run Goals Jan 2022

Foreign Exchange Market

Energy Complex

The Baker Hughes rig count was up 1 this week. There are 632 oil and gas rigs operating in the US – Down 127 from last year.

Metals Complex

Employment Picture

Weekly Unemployment Claims – Released Thursday 9/7/2023 –In the week ending September 2, the advance figure for seasonally adjusted initial claims was 216,000 decreasing 13,000 from the previous week’s revised level. The 4-week moving average was 229,250 a decrease of 8,500 from the previous week’s revised average.

August Jobs Report – BLS Summary – Released 9/1/2023 – The US Economy added 187k nonfarm jobs in August and the Unemployment rate edged up to 3.8%. Average hourly earnings increased 8 cents to $33.82. Hiring highlights include +102k Education and Health Services, +40k Leisure and Hospitality, and +22k Construction.

Job Openings & Labor Turnover Survey JOLTS – Released 8/29/2023 – The number of job openings decreased to 8.8 million on the last business day of July, the U.S. Bureau of Labor Statistics reported. Over the month the number of hires and total separations were little changed at 5.8 million and 5.5 million, respectively. Within separations, quits (3.5 million) decreased and discharges (1.6 million) changed little.

Employment Cost Index – Released 7/28/2023 – Compensation costs for civilian workers increased 1.0% for the 3-month period ending in June 2023. The 12-month period ending in June 2023 saw compensation costs increase by 4.5. The 12-month period ending June 2022 increased 5.1%. Wages and salaries increased 4.6 percent over the 12-month June 2023 and increased 5.3 percent for the 12-month period ending in June 2022. Benefit costs increased 4.2 percent over the 12-month period ending June 2023 and increased 4.8 percent for the 12-month period ending in June 2022. This report is published quarterly.

This Week’s Economic Data

Links take you to the data source

Consumer Credit – Released 9/8/2023 – Consumer credit increased at a seasonally adjusted annual rate of 2.5 percent in July. Revolving credit increased at an annual rate of 9.2 percent, while nonrevolving credit increased at an annual rate of 0.2 percent.

U.S. Trade Balance – Released 9/6/2023 – The U.S. Census Bureau and the U.S. Bureau of Economic Analysis announced that the goods and services deficit was $65.0 billion in July, up $1.3 billion from $63.7 billion in June. June exports were $251.7 billion, $3.9 billion more than June exports. July imports were $316.7 billion, $5.2 billion more than June imports. The July increase in the goods and services deficit reflected an increase in the goods deficit of $2.0 billion to $90.0 billion and an increase in the services surplus of $0.7 billion to $25.0 billion.

PMI Non-Manufacturing Index – Released 9/5/2023 – Economic activity in the services sector expanded in August for the eighth consecutive month as the Services PMI® registered 54.5 percent, 1.8 percentage point higher than July’s reading of 52.7 percent.

Recent Economic Data

Links take you to the data source

U.S. Construction Spending– Released 9/1/2023 – Construction spending during July 2023 was estimated at a seasonally adjusted annual rate of $1,972.6 billion, 0.7 percent above the revised June estimate of $1,958.9 billion. The July figure is 5.5 percent above the July 2022 estimate of $1,869.3 billion.

PMI Manufacturing Index – Released 9/1/2023 – The August Manufacturing PMI registered 47.6 percent, 1.2 percentage points higher than the 46.4 percent recorded in July. Regarding the overall economy, this figure indicates a ninth month of contraction after a 30-month period of expansion. The New Orders Index remained in contraction territory at 46.8 percent, 0.5 percentage points lower than the figure of 47.3 percent recorded in July. The Production Index reading of 50.0 percent is a 1.7-percentage point increase compared to July’s figure of 48.3 percent.

US Light Vehicle Sales– Released 8/31/2023 – U.S. light vehicle sales were at a seasonally adjusted annual rate (SAAR) of 15.732 million units in August.

Chicago PMI – Released 8/31/2023 – Chicago PMI remained in contraction territory in August increasing to 48.7 points up from 42.8 points in August. This increase surpassed expectations but still marks twelve months in contractionary territory.

Personal Income – Released 8/31/2023 – Personal income increased $45.0 billion (0.2 percent at a monthly rate) in July. Disposable personal income (DPI) increased $7.3 billion (0.1 percent). Personal consumption expenditures (PCE) increased $144.6 billion (0.8 percent).

Second Estimate of 2nd Quarter 2023 GDP – Released 8/30/2023 – Real gross domestic product (GDP) increased at an annual rate of 2.1 percent in the second quarter of 2023, according to the “second” estimate released by the Bureau of Economic Analysis. The GDP estimate released today is based on more complete source data than were available for the “advance” estimate issued last month which had GDP increasing at 2.4 percent. In the first quarter, real GDP increased 2.0 percent. The increase in real GDP reflected increases in consumer spending, nonresidential fixed investment, state and local government spending, private inventory investment, and federal government spending that were partly offset by decreases in exports and residential fixed investment. Imports, which are a subtraction in the calculation of GDP, decreased.The updated estimates primarily reflected downward revisions to private inventory investment and nonresidential fixed investment that were partly offset by an upward revision to state and local government spending.

Consumer Confidence– Released 8/29/2023 – Consumer Confidence decreased in August to 106.1, down from 114.0 in July. August’s decline reflected dips in both the current conditions and expectations indexes. Consumers were once again preoccupied with rising prices in general, and for groceries and gasoline in particular.

Durable Goods Released 8/24/2023 – New orders for manufactured durable goods in July, down following four consecutive months of increases, decreased $15.5 billion or 5.2 percent to $285.9 billion, the U.S. Census Bureau announced today. This followed a 4.4 percent June increase. Excluding transportation, new orders increased 0.5 percent. Excluding defense, new orders decreased 5.4 percent. Transportation equipment, also down following four consecutive months of increases, drove the decrease, $16.4 billion or 14.3 percent to $98.7 billion.

New Residential Sales Released 8/23/2023 – Sales of new single‐family houses in July 2023 were at a seasonally adjusted annual rate of 714,000, according to estimates released jointly by the U.S. Census Bureau and the Department of Housing and Urban Development. This is 4.4 percent above the revised June rate of 684,000 and is 31.5 percent above the July 2022 estimate of 543,000. The median sales price of new houses sold in July 2023 was $436,700. The average sales price was $513,000. At the end of July, the seasonally adjusted estimate of new homes for sale was 437,000, a supply of 7.3 months at the current sales rate.

Existing Home Sales Released 8/22/2023 – July 2023 brought 4.07 million in sales, a decrease of 2.2% from June. The median sales price was $406,700. The current unsold housing inventory was 3.3 months of inventory.

Housing Starts– Released 8/16/2023 – July housing starts came in at 1,452,000, 3.9% above the June estimate and 5.9% above the July 2022 rate. Building permits were 0.1% above the June rate at $1,441,000 and 13.0% below the July 2022 rate.

Industrial Production and Capacity Utilization Released 8/16/2023 – Industrial production increased 1.0% in July following two months of decline. Utilities output increased 5.4%. Manufacturing increased 0.5%. Mining increased 0.5%. Capacity utilization increased to 79.3% in July, 0.4% below the long-run average.

Retail Sales– Released 8/15/2023 – Headline retail sales increased 0.7% in July and are up 3.2% above July 2022.

Producer Price Index – Released 8/11/2023 – The Producer Price Index for final demand increased 0.3 percent in July, seasonally adjusted. Final demand were unchanged in June and decreased 0.3 in May. On an unadjusted basis, the index for final demand moved up 0.8 percent for the 12 months ended in July.

Consumer Price Index – Released 8/10/2023 – The Consumer Price Index for All Urban Consumers rose 0.2 percent in July on a seasonally adjusted basis, after increasing 0.2 percent in June. Over the last 12 months, the all items index increased 3.2 percent before seasonal adjustment.

Next week we get data on CPI, PPI, Retail Sales, Industrial Production and Capacity Utilization.

Data Sources:

Bureau of Economic Analysis (BEA)

Congressional Budget Office (CBO)

U.S. Bureau of Labor Statistics (BLS)

Federal Reserve Economic Data (FRED Charts)

CME Fed Watch

U.S. Treasury – Yields

U.S. Census Bureau

Institute for Supply Management (ISM)

Weekly DOL Employment Data

BLS Monthly Jobs Report

JOLTS

US Energy Admin (EIA)

BLS Consumer Price Index CPI

BLS Producer Price Index PPI

Atlanta Fed GDPNOW

NY Fed Nowcast GDP

US Census Bureau Housing Starts

Consumer Credit

USCB Retail Sales

Construction Spending

Federal Reserve Dot Plots

NY Empire Index

Philadelphia Federal Reserve

P/E Ratio Data -Yardeni Research

Technical Analysis Info:

StockCharts.com – Financial Charts

Exponential vs Simple moving average

Koyfin.com

Other Links:

1973 Arab Oil Embargo

Hunt Brothers Silver

Long-Term Capital bailout

Asian Contagion

Categories:

Tags: