Weekly Market Update | Week 35

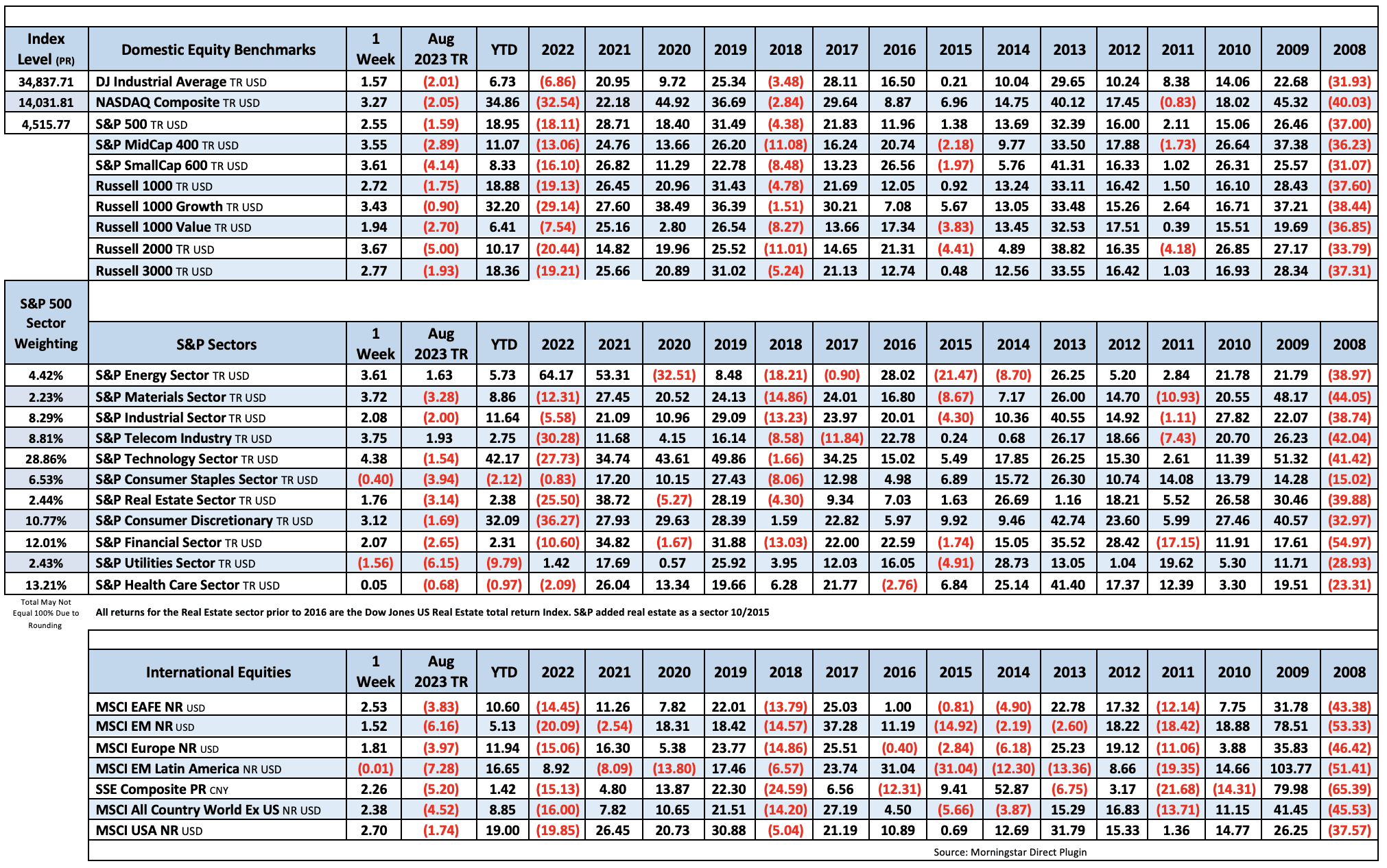

Stocks closed higher this week but ended the month lower overall. The S&P 500 and Nasdaq suffered their first monthly declines since February. Treasuries were mostly weaker with the curve bear steepening, though yields finished well off their highs thanks to a late-month reprieve. Two-year yields fell slightly, down 2bps at 4.85% while ten-year yields rose 15 bp to 4.10% after trading as high as 4.34% at one point, the highest since before the GFC. The 30 year yield jumped 18 bps closing August at 4.20% (and jumping Friday by another 9bps). The dollar index gained 1.7%, reversing a good chunk of the prior two months’ losses. Gold fell more than 2%. WTI crude gained 2.2% for a third straight monthly gain.

It was a mixed month for the “Magnificent Seven” megacap tech+ names that drove nearly 75% of the S&P’s gains in 1H and extended their rally in July. NVDA +5.6% was the standout with help from another blowout earnings report and guidance that beat a very higher. AMZN +3.2% was another post-earnings standout with help from an AWS beat, while GOOGL +2.6% also found some AI support. META (7.1%), AAPL (4.4%), TSLA (3.5%) and MSFT (2.4%) underperformed.

One of the more prominent headwinds facing stocks in August was the rise of the 10 year yield despite the broader disinflation narrative. The bond yield backup was chalked up to myriad factors, including another repricing of Fed pivot expectations on the better US growth outlook, heightened deficit scrutiny following the Fitch downgrade, supply pressures and peak disinflation chatter.

China growth concerns also played a role in the August pullback. July activity, credit and deflation data all came in weaker than expected. The structural pressures facing the property sector continued to attract outsized scrutiny, along with fragile consumer confidence. In addition, policy response measures continued to largely underwhelm and President Xi specifically pushed back against calls for more direct consumer stimulus.

The corporate calendar presented some select problems for sentiment. AAPL (4.4%) missed on Jun Q iPhone revenues and underwhelmed with guidance for Sep Q revenue to be down similar to the 1% y/y decline in the Jun Q. Weaker guidance from UPS (9.5%) put some additional focus on negative operating leverage risk (via wage pressures) for earnings. Department stores flagged some issues with credit delinquencies, while shrink (theft) was repeatedly mentioned by retailers as a profit drag.

There were a number of other bearish talking points in August. These included bank credit ratings downgrades/downgrade warnings, further tightening of bank lending standards and softening of loan demand, a looming potential UAW strike, highest mortgage rates since 2001, lowest home purchase applications since 1995, near-record late summer gas prices and more research suggesting consumers have largely exhausted their excess savings.

Despite the pullback, there were a number of positive developments, particularly in terms of the continued disinflation traction and positive macro surprise momentum that further underpinned soft-landing expectations. In addition, earnings season ended with a beat rate above the five-year average, earnings revisions breadth turned higher, labor market loosening was seen through lower job openings rather than job cuts, and there were still no signs of a credit crunch in the NFIB small business optimism index.

In addition, August ended on an upbeat note with risk sentiment underpinned by a meaningful rate reprieve, favorable positioning dynamics (systematic funds flipped back into buy mode), renewed AI hype tailwind, flurry of China stimulus measures, pickup in M&A headlines, and talk that adverse September seasonality may have been pulled forward (or negated with the double-digit ytd % gains).

The monthly jobs report came out Friday, it showed the economy added 187k jobs in August while June and July were revised down a combination of 110k. The unemployment rate rose to 3.8% in August, up from 3.5% in July—reflecting more Americans seeking work.

Fixed Income

Yield Curve

July FOMC Statement July Fed Minutes Balance Sheet Reduction Plan Credit, Liquidity and Balance Sheet Federal Reserve Dot Plots

Treasury.gov yields FOMC Policy Normalization Statement Longer- Run Goals Jan 2022

Foreign Exchange Market

Energy Complex

The Baker Hughes rig count was down 1 this week. There are 631 oil and gas rigs operating in the US – Down 129 from last year.

Metals Complex

Employment Picture

August Jobs Report – BLS Summary – Released 9/1/2023 – The US Economy added 187k nonfarm jobs in August and the Unemployment rate edged up to 3.8%. Average hourly earnings increased 8 cents to $33.82. Hiring highlights include +102k Education and Health Services, +40k Leisure and Hospitality, and +22k Construction.

- Average hourly earnings increased 8 cents/0.2% to $33.82.

- U3 unemployment rate increased 0.3% to 3.8%. U6 unemployment rate increased 0.4% to 7.1%.

- The labor force participation rate increased by 0.2% to 62.8%.

- Average work week increased 0.1 hours to 34.4 hours.

Weekly Unemployment Claims – Released Thursday 8/31/2023 – In the week ending August 26, the advance figure for seasonally adjusted initial claims was 228,000 decreasing 4,000 from the previous week’s revised level. The 4-week moving average was 237,500 an increase of 250 from the previous week’s revised average.

Job Openings & Labor Turnover Survey JOLTS – Released 8/29/2023 – The number of job openings decreased to 8.8 million on the last business day of July, the U.S. Bureau of Labor Statistics reported. Over the month the number of hires and total separations were little changed at 5.8 million and 5.5 million, respectively. Within separations, quits (3.5 million) decreased and discharges (1.6 million) changed little.

Employment Cost Index – Released 7/28/2023 – Compensation costs for civilian workers increased 1.0% for the 3-month period ending in June 2023. The 12-month period ending in June 2023 saw compensation costs increase by 4.5. The 12-month period ending June 2022 increased 5.1%. Wages and salaries increased 4.6 percent over the 12-month June 2023 and increased 5.3 percent for the 12-month period ending in June 2022. Benefit costs increased 4.2 percent over the 12-month period ending June 2023 and increased 4.8 percent for the 12-month period ending in June 2022. This report is published quarterly.

This Week’s Economic Data

Links take you to the data source

U.S. Construction Spending – Released 9/1/2023 – Construction spending during July 2023 was estimated at a seasonally adjusted annual rate of $1,972.6 billion, 0.7 percent above the revised June estimate of $1,958.9 billion. The July figure is 5.5 percent above the July 2022 estimate of $1,869.3 billion.

PMI Manufacturing Index – Released 9/1/2023 – The August Manufacturing PMI registered 47.6 percent, 1.2 percentage points higher than the 46.4 percent recorded in July. Regarding the overall economy, this figure indicates a ninth month of contraction after a 30-month period of expansion. The New Orders Index remained in contraction territory at 46.8 percent, 0.5 percentage points lower than the figure of 47.3 percent recorded in July. The Production Index reading of 50.0 percent is a 1.7-percentage point increase compared to July’s figure of 48.3 percent.

Chicago PMI – Released 8/31/2023 – Chicago PMI remained in contraction territory in August increasing to 48.7 points up from 42.8 points in August. This increase surpassed expectations but still marks twelve months in contractionary territory.

Personal Income – Released 8/31/2023 – Personal income increased $45.0 billion (0.2 percent at a monthly rate) in July. Disposable personal income (DPI) increased $7.3 billion (0.1 percent). Personal consumption expenditures (PCE) increased $144.6 billion (0.8 percent).

Second Estimate of 2nd Quarter 2023 GDP – Released 8/30/2023 – Real gross domestic product (GDP) increased at an annual rate of 2.1 percent in the second quarter of 2023, according to the “second” estimate released by the Bureau of Economic Analysis. The GDP estimate released today is based on more complete source data than were available for the “advance” estimate issued last month which had GDP increasing at 2.4 percent. In the first quarter, real GDP increased 2.0 percent. The increase in real GDP reflected increases in consumer spending, nonresidential fixed investment, state and local government spending, private inventory investment, and federal government spending that were partly offset by decreases in exports and residential fixed investment. Imports, which are a subtraction in the calculation of GDP, decreased. The updated estimates primarily reflected downward revisions to private inventory investment and nonresidential fixed investment that were partly offset by an upward revision to state and local government spending.

Consumer Confidence – Released 8/29/2023 – Consumer Confidence decreased in August to 106.1, down from 114.0 in July. August’s decline reflected dips in both the current conditions and expectations indexes. Consumers were once again preoccupied with rising prices in general, and for groceries and gasoline in particular.

Recent Economic Data

Links take you to the data source

Durable Goods – Released 8/24/2023 – New orders for manufactured durable goods in July, down following four consecutive months of increases, decreased $15.5 billion or 5.2 percent to $285.9 billion, the U.S. Census Bureau announced today. This followed a 4.4 percent June increase. Excluding transportation, new orders increased 0.5 percent. Excluding defense, new orders decreased 5.4 percent. Transportation equipment, also down following four consecutive months of increases, drove the decrease, $16.4 billion or 14.3 percent to $98.7 billion.

New Residential Sales – Released 8/23/2023 – Sales of new single‐family houses in July 2023 were at a seasonally adjusted annual rate of 714,000, according to estimates released jointly by the U.S. Census Bureau and the Department of Housing and Urban Development. This is 4.4 percent above the revised June rate of 684,000 and is 31.5 percent above the July 2022 estimate of 543,000. The median sales price of new houses sold in July 2023 was $436,700. The average sales price was $513,000. At the end of July, the seasonally adjusted estimate of new homes for sale was 437,000, a supply of 7.3 months at the current sales rate.

Existing Home Sales – Released 8/22/2023 – July 2023 brought 4.07 million in sales, a decrease of 2.2% from June. The median sales price was $406,700. The current unsold housing inventory was 3.3 months of inventory.

Housing Starts – Released 8/16/2023 – July housing starts came in at 1,452,000, 3.9% above the June estimate and 5.9% above the July 2022 rate. Building permits were 0.1% above the June rate at $1,441,000 and 13.0% below the July 2022 rate.

Industrial Production and Capacity Utilization – Released 8/16/2023 – Industrial production increased 1.0% in July following two months of decline. Utilities output increased 5.4%. Manufacturing increased 0.5%. Mining increased 0.5%. Capacity utilization increased to 79.3% in July, 0.4% below the long-run average.

Retail Sales – Released 8/15/2023 – Headline retail sales increased 0.7% in July and are up 3.2% above July 2022.

Producer Price Index – Released 8/11/2023 – The Producer Price Index for final demand increased 0.3 percent in July, seasonally adjusted. Final demand were unchanged in June and decreased 0.3 in May. On an unadjusted basis, the index for final demand moved up 0.8 percent for the 12 months ended in July.

Consumer Price Index –Released 8/10/2023 – The Consumer Price Index for All Urban Consumers rose 0.2 percent in July on a seasonally adjusted basis, after increasing 0.2 percent in June. Over the last 12 months, the all items index increased 3.2 percent before seasonal adjustment.

U.S. Trade Balance – Released 8/8/2023 – The U.S. Census Bureau and the U.S. Bureau of Economic Analysis announced that the goods and services deficit was $65.5 billion in June, down $2.8 billion from $68.3 billion in May. June exports were $247.5 billion, $0.3 billion less than May exports. June imports were $313.0 billion, $3.1 billion less than May imports. The June decrease in the goods and services deficit reflected a decrease in the goods deficit of $2.8 billion to $88.2 billion and a decrease in the services surplus of less than $0.1 billion to $22.7 billion.

Consumer Credit – Released 8/7/2023 – Consumer credit increased at a seasonally adjusted annual rate of 4 percent in the second quarter. Revolving credit increased at an annual rate of 7.1 percent, while nonrevolving credit increased at an annual rate of 3.0 percent. Consumer credit increased at a seasonally adjusted annual rate of 4.3 percent in June.

US Light Vehicle Sales – Released 8/4/2023 – U.S. light vehicle sales were at a seasonally adjusted annual rate (SAAR) of 15.735 million units in July.

PMI Non-Manufacturing Index – Released 8/3/2023 – Economic activity in the services sector expanded in July for the seventh consecutive month as the Services PMI® registered 52.7 percent, 1.2 percentage point lower than June’s reading of 53.9 percent.

Next week we get data on Services PMI, Consumer Credit, and the U.S. Trade Balance.

Data Sources:

Bureau of Economic Analysis (BEA)

Congressional Budget Office (CBO)

U.S. Bureau of Labor Statistics (BLS)

Federal Reserve Economic Data (FRED Charts)

CME Fed Watch

U.S. Treasury – Yields

U.S. Census Bureau

Institute for Supply Management (ISM)

Weekly DOL Employment Data

BLS Monthly Jobs Report

JOLTS

US Energy Admin (EIA)

BLS Consumer Price Index CPI

BLS Producer Price Index PPI

Atlanta Fed GDPNOW

NY Fed Nowcast GDP

US Census Bureau Housing Starts

Consumer Credit

USCB Retail Sales

Construction Spending

Federal Reserve Dot Plots

NY Empire Index

Philadelphia Federal Reserve

P/E Ratio Data -Yardeni Research

Technical Analysis Info:

StockCharts.com – Financial Charts

Exponential vs Simple moving average

Koyfin.com

Other Links:

1973 Arab Oil Embargo

Hunt Brothers Silver

Long-Term Capital bailout

Asian Contagion

Week 35 Talking Points

Table of Contents

Weekly Market Update | Week 35

Stocks closed higher this week but ended the month lower overall. The S&P 500 and Nasdaq suffered their first monthly declines since February. Treasuries were mostly weaker with the curve bear steepening, though yields finished well off their highs thanks to a late-month reprieve. Two-year yields fell slightly, down 2bps at 4.85% while ten-year yields rose 15 bp to 4.10% after trading as high as 4.34% at one point, the highest since before the GFC. The 30 year yield jumped 18 bps closing August at 4.20% (and jumping Friday by another 9bps). The dollar index gained 1.7%, reversing a good chunk of the prior two months’ losses. Gold fell more than 2%. WTI crude gained 2.2% for a third straight monthly gain.

It was a mixed month for the “Magnificent Seven” megacap tech+ names that drove nearly 75% of the S&P’s gains in 1H and extended their rally in July. NVDA +5.6% was the standout with help from another blowout earnings report and guidance that beat a very higher. AMZN +3.2% was another post-earnings standout with help from an AWS beat, while GOOGL +2.6% also found some AI support. META (7.1%), AAPL (4.4%), TSLA (3.5%) and MSFT (2.4%) underperformed.

One of the more prominent headwinds facing stocks in August was the rise of the 10 year yield despite the broader disinflation narrative. The bond yield backup was chalked up to myriad factors, including another repricing of Fed pivot expectations on the better US growth outlook, heightened deficit scrutiny following the Fitch downgrade, supply pressures and peak disinflation chatter.

China growth concerns also played a role in the August pullback. July activity, credit and deflation data all came in weaker than expected. The structural pressures facing the property sector continued to attract outsized scrutiny, along with fragile consumer confidence. In addition, policy response measures continued to largely underwhelm and President Xi specifically pushed back against calls for more direct consumer stimulus.

The corporate calendar presented some select problems for sentiment. AAPL (4.4%) missed on Jun Q iPhone revenues and underwhelmed with guidance for Sep Q revenue to be down similar to the 1% y/y decline in the Jun Q. Weaker guidance from UPS (9.5%) put some additional focus on negative operating leverage risk (via wage pressures) for earnings. Department stores flagged some issues with credit delinquencies, while shrink (theft) was repeatedly mentioned by retailers as a profit drag.

There were a number of other bearish talking points in August. These included bank credit ratings downgrades/downgrade warnings, further tightening of bank lending standards and softening of loan demand, a looming potential UAW strike, highest mortgage rates since 2001, lowest home purchase applications since 1995, near-record late summer gas prices and more research suggesting consumers have largely exhausted their excess savings.

Despite the pullback, there were a number of positive developments, particularly in terms of the continued disinflation traction and positive macro surprise momentum that further underpinned soft-landing expectations. In addition, earnings season ended with a beat rate above the five-year average, earnings revisions breadth turned higher, labor market loosening was seen through lower job openings rather than job cuts, and there were still no signs of a credit crunch in the NFIB small business optimism index.

In addition, August ended on an upbeat note with risk sentiment underpinned by a meaningful rate reprieve, favorable positioning dynamics (systematic funds flipped back into buy mode), renewed AI hype tailwind, flurry of China stimulus measures, pickup in M&A headlines, and talk that adverse September seasonality may have been pulled forward (or negated with the double-digit ytd % gains).

The monthly jobs report came out Friday, it showed the economy added 187k jobs in August while June and July were revised down a combination of 110k. The unemployment rate rose to 3.8% in August, up from 3.5% in July—reflecting more Americans seeking work.

Fixed Income

Yield Curve

July FOMC Statement July Fed Minutes Balance Sheet Reduction Plan Credit, Liquidity and Balance Sheet Federal Reserve Dot Plots

Treasury.gov yields FOMC Policy Normalization Statement Longer- Run Goals Jan 2022

Foreign Exchange Market

Energy Complex

The Baker Hughes rig count was down 1 this week. There are 631 oil and gas rigs operating in the US – Down 129 from last year.

Metals Complex

Employment Picture

August Jobs Report – BLS Summary – Released 9/1/2023 – The US Economy added 187k nonfarm jobs in August and the Unemployment rate edged up to 3.8%. Average hourly earnings increased 8 cents to $33.82. Hiring highlights include +102k Education and Health Services, +40k Leisure and Hospitality, and +22k Construction.

Weekly Unemployment Claims – Released Thursday 8/31/2023 – In the week ending August 26, the advance figure for seasonally adjusted initial claims was 228,000 decreasing 4,000 from the previous week’s revised level. The 4-week moving average was 237,500 an increase of 250 from the previous week’s revised average.

Job Openings & Labor Turnover Survey JOLTS – Released 8/29/2023 – The number of job openings decreased to 8.8 million on the last business day of July, the U.S. Bureau of Labor Statistics reported. Over the month the number of hires and total separations were little changed at 5.8 million and 5.5 million, respectively. Within separations, quits (3.5 million) decreased and discharges (1.6 million) changed little.

Employment Cost Index – Released 7/28/2023 – Compensation costs for civilian workers increased 1.0% for the 3-month period ending in June 2023. The 12-month period ending in June 2023 saw compensation costs increase by 4.5. The 12-month period ending June 2022 increased 5.1%. Wages and salaries increased 4.6 percent over the 12-month June 2023 and increased 5.3 percent for the 12-month period ending in June 2022. Benefit costs increased 4.2 percent over the 12-month period ending June 2023 and increased 4.8 percent for the 12-month period ending in June 2022. This report is published quarterly.

This Week’s Economic Data

Links take you to the data source

U.S. Construction Spending – Released 9/1/2023 – Construction spending during July 2023 was estimated at a seasonally adjusted annual rate of $1,972.6 billion, 0.7 percent above the revised June estimate of $1,958.9 billion. The July figure is 5.5 percent above the July 2022 estimate of $1,869.3 billion.

PMI Manufacturing Index – Released 9/1/2023 – The August Manufacturing PMI registered 47.6 percent, 1.2 percentage points higher than the 46.4 percent recorded in July. Regarding the overall economy, this figure indicates a ninth month of contraction after a 30-month period of expansion. The New Orders Index remained in contraction territory at 46.8 percent, 0.5 percentage points lower than the figure of 47.3 percent recorded in July. The Production Index reading of 50.0 percent is a 1.7-percentage point increase compared to July’s figure of 48.3 percent.

Chicago PMI – Released 8/31/2023 – Chicago PMI remained in contraction territory in August increasing to 48.7 points up from 42.8 points in August. This increase surpassed expectations but still marks twelve months in contractionary territory.

Personal Income – Released 8/31/2023 – Personal income increased $45.0 billion (0.2 percent at a monthly rate) in July. Disposable personal income (DPI) increased $7.3 billion (0.1 percent). Personal consumption expenditures (PCE) increased $144.6 billion (0.8 percent).

Second Estimate of 2nd Quarter 2023 GDP – Released 8/30/2023 – Real gross domestic product (GDP) increased at an annual rate of 2.1 percent in the second quarter of 2023, according to the “second” estimate released by the Bureau of Economic Analysis. The GDP estimate released today is based on more complete source data than were available for the “advance” estimate issued last month which had GDP increasing at 2.4 percent. In the first quarter, real GDP increased 2.0 percent. The increase in real GDP reflected increases in consumer spending, nonresidential fixed investment, state and local government spending, private inventory investment, and federal government spending that were partly offset by decreases in exports and residential fixed investment. Imports, which are a subtraction in the calculation of GDP, decreased. The updated estimates primarily reflected downward revisions to private inventory investment and nonresidential fixed investment that were partly offset by an upward revision to state and local government spending.

Consumer Confidence – Released 8/29/2023 – Consumer Confidence decreased in August to 106.1, down from 114.0 in July. August’s decline reflected dips in both the current conditions and expectations indexes. Consumers were once again preoccupied with rising prices in general, and for groceries and gasoline in particular.

Recent Economic Data

Links take you to the data source

Durable Goods – Released 8/24/2023 – New orders for manufactured durable goods in July, down following four consecutive months of increases, decreased $15.5 billion or 5.2 percent to $285.9 billion, the U.S. Census Bureau announced today. This followed a 4.4 percent June increase. Excluding transportation, new orders increased 0.5 percent. Excluding defense, new orders decreased 5.4 percent. Transportation equipment, also down following four consecutive months of increases, drove the decrease, $16.4 billion or 14.3 percent to $98.7 billion.

New Residential Sales – Released 8/23/2023 – Sales of new single‐family houses in July 2023 were at a seasonally adjusted annual rate of 714,000, according to estimates released jointly by the U.S. Census Bureau and the Department of Housing and Urban Development. This is 4.4 percent above the revised June rate of 684,000 and is 31.5 percent above the July 2022 estimate of 543,000. The median sales price of new houses sold in July 2023 was $436,700. The average sales price was $513,000. At the end of July, the seasonally adjusted estimate of new homes for sale was 437,000, a supply of 7.3 months at the current sales rate.

Existing Home Sales – Released 8/22/2023 – July 2023 brought 4.07 million in sales, a decrease of 2.2% from June. The median sales price was $406,700. The current unsold housing inventory was 3.3 months of inventory.

Housing Starts – Released 8/16/2023 – July housing starts came in at 1,452,000, 3.9% above the June estimate and 5.9% above the July 2022 rate. Building permits were 0.1% above the June rate at $1,441,000 and 13.0% below the July 2022 rate.

Industrial Production and Capacity Utilization – Released 8/16/2023 – Industrial production increased 1.0% in July following two months of decline. Utilities output increased 5.4%. Manufacturing increased 0.5%. Mining increased 0.5%. Capacity utilization increased to 79.3% in July, 0.4% below the long-run average.

Retail Sales – Released 8/15/2023 – Headline retail sales increased 0.7% in July and are up 3.2% above July 2022.

Producer Price Index – Released 8/11/2023 – The Producer Price Index for final demand increased 0.3 percent in July, seasonally adjusted. Final demand were unchanged in June and decreased 0.3 in May. On an unadjusted basis, the index for final demand moved up 0.8 percent for the 12 months ended in July.

Consumer Price Index –Released 8/10/2023 – The Consumer Price Index for All Urban Consumers rose 0.2 percent in July on a seasonally adjusted basis, after increasing 0.2 percent in June. Over the last 12 months, the all items index increased 3.2 percent before seasonal adjustment.

U.S. Trade Balance – Released 8/8/2023 – The U.S. Census Bureau and the U.S. Bureau of Economic Analysis announced that the goods and services deficit was $65.5 billion in June, down $2.8 billion from $68.3 billion in May. June exports were $247.5 billion, $0.3 billion less than May exports. June imports were $313.0 billion, $3.1 billion less than May imports. The June decrease in the goods and services deficit reflected a decrease in the goods deficit of $2.8 billion to $88.2 billion and a decrease in the services surplus of less than $0.1 billion to $22.7 billion.

Consumer Credit – Released 8/7/2023 – Consumer credit increased at a seasonally adjusted annual rate of 4 percent in the second quarter. Revolving credit increased at an annual rate of 7.1 percent, while nonrevolving credit increased at an annual rate of 3.0 percent. Consumer credit increased at a seasonally adjusted annual rate of 4.3 percent in June.

US Light Vehicle Sales – Released 8/4/2023 – U.S. light vehicle sales were at a seasonally adjusted annual rate (SAAR) of 15.735 million units in July.

PMI Non-Manufacturing Index – Released 8/3/2023 – Economic activity in the services sector expanded in July for the seventh consecutive month as the Services PMI® registered 52.7 percent, 1.2 percentage point lower than June’s reading of 53.9 percent.

Next week we get data on Services PMI, Consumer Credit, and the U.S. Trade Balance.

Data Sources:

Bureau of Economic Analysis (BEA)

Congressional Budget Office (CBO)

U.S. Bureau of Labor Statistics (BLS)

Federal Reserve Economic Data (FRED Charts)

CME Fed Watch

U.S. Treasury – Yields

U.S. Census Bureau

Institute for Supply Management (ISM)

Weekly DOL Employment Data

BLS Monthly Jobs Report

JOLTS

US Energy Admin (EIA)

BLS Consumer Price Index CPI

BLS Producer Price Index PPI

Atlanta Fed GDPNOW

NY Fed Nowcast GDP

US Census Bureau Housing Starts

Consumer Credit

USCB Retail Sales

Construction Spending

Federal Reserve Dot Plots

NY Empire Index

Philadelphia Federal Reserve

P/E Ratio Data -Yardeni Research

Technical Analysis Info:

StockCharts.com – Financial Charts

Exponential vs Simple moving average

Koyfin.com

Other Links:

1973 Arab Oil Embargo

Hunt Brothers Silver

Long-Term Capital bailout

Asian Contagion

Categories:

Tags: