Good Life Advisors – Talking Points – Week 12

The 2nd quarter WAM rebalance is coming up Monday, April 3rd. The client-approved model updates and summary outlook will be out tomorrow 3/27. The larger quarterly commentary is coming soon.

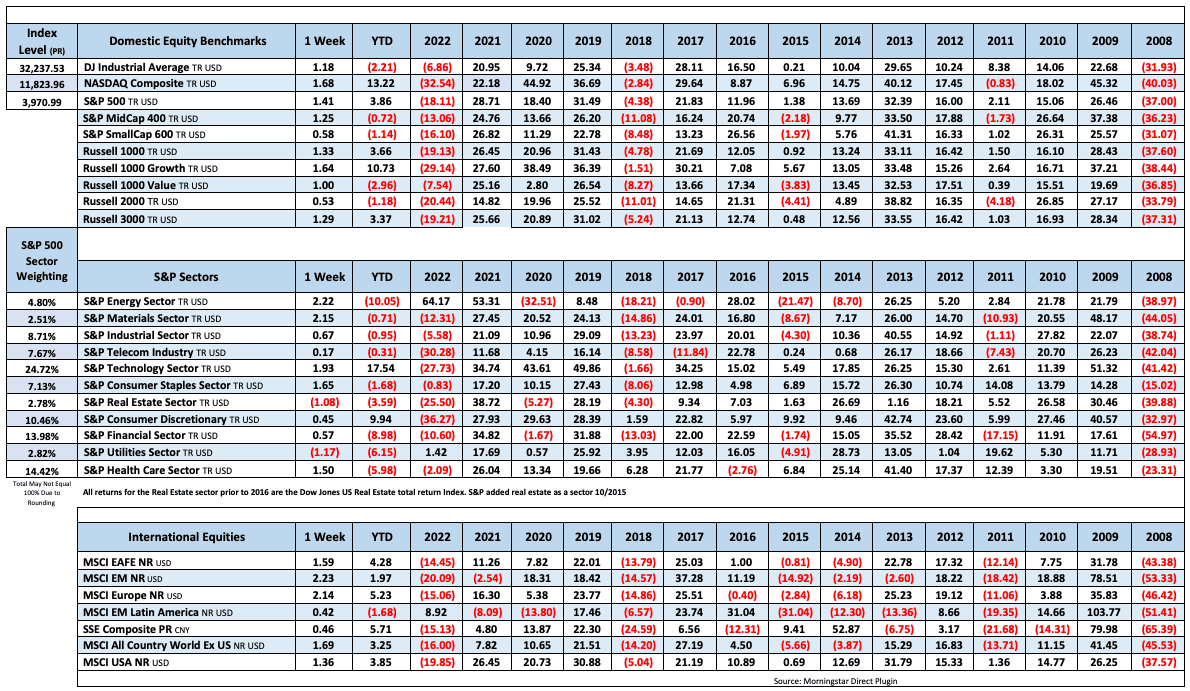

Equities ended the week modestly higher despite a very bumpy ride. Most of the focus was on banking sector and the Federal Reserve. Investors are on lookout for any contagion and attempting to gauge the fallout after the FDIC takeover of SVB and Signature two weeks ago. In response, the KBW Bank Index fell for a third-straight week and is now down nearly 29% for the month, on pace for the worst monthly performance since January 2009. Outside the states, UBS agreed to take over its longtime Swiss rival Credit Suisse for a paltry $3 billion. This led to some stabilization initially, but there are still major worries about Deutsche Bank, Germany’s largest.

The March FOMC meeting ended with a unanimous 25 bp rate hike. Headed into the meeting, markets expected a ~90% chance of a 25 bp hike, with a 10% chance for a pause. However, the policy statement changed the language around future increases, which now reads “some additional policy firming may be appropriate.” The updated Summary of Economic Projections also showed the 2023 median dot of 5.1%, unchanged from the December projection. There were also no changes to the balance sheet runoff as some previews suggested. In the post-meeting press conference, Chair Powell said credit tightening could have the same impact as Fed policy, though some economists cautioned of upside risk to the policy path if bank stresses subside. Powell also played down rate cuts, saying Fed officials generally don’t expect rate cuts this year. While markets sold off following the meeting on rate cut pushback (and Treasury Secretary’s simultaneous commentary pushing back against blanket deposit guarantees), a Thursday rally was tabbed to what some economists said was a dovish hike. Markets see the current fed funds rate as the peak and expect between 100 and 125 bp of rate cuts by year-end.

There was mixed messaging around deposit guarantees and FDIC insurance as Treasury Secretary Yellen said she has not considered blanket insurance for US banking deposits without approval from Congress. These comments diverged from Fed Chair Powell, who was speaking simultaneously and said that depositors should assume that their deposits are safe (though Yellen changed her opening statement on Thursday’s hearing to say Treasury is prepared to take additional actions if warranted). However, a blanket guarantee would fall on Congress and not Treasury, though Bloomberg noted this week Senate Banking Chair Brown said prospects around lifting the FDIC cap are improving. The Senate Banking Committee is set to hold hearings on the collapse of SVB and Signature Bank this coming week.

There was a big focus this week on the rally across tech. The Goldman Sachs trading desk highlighted the continued MF rotation out of cyclicals and into supercap tech (where they have been underweight for an extended period of time), and noted that Nasdaq has now outperformed the equal-weight S&P by >10pts in March, the second biggest monthly spread in ~20 years. A number of press articles highlighted the FOMO around a Fed pivot, with managers not wanting to lose out on potential returns if the market rallies. However, central bank tightening remains a key risk with major central banks continuing to push ahead with rate hikes despite tighter financial conditions and bank turmoil. There are also growing concerns around commercial real estate. FT noted CRE loans make up 43% of small bank total lending vs 13% for the biggest banks, putting further scrutiny on regional banks.

Fixed Income

Yield Curve

The current banking situation may have been the catalyst for 10 minus two inversion to start its way back to a positive spread.

January FOMC Statement January Fed Minutes Balance Sheet Reduction Plan Credit, Liquidity and Balance Sheet Federal Reserve Dot Plots

Treasury.gov yields FOMC Policy Normalization Statement Longer- Run Goals Jan 2022

Foreign Exchange Market

Energy Complex

The Baker Hughes rig count was up by 4 this week. There are 758 oil and gas rigs operating in the US – Up 88 over last year.

Metals Complex

Employment Picture

Weekly Unemployment Claims – Released Thursday 3/23/2023 – The week ending March 18th observed a decrease of 1k in initial claims decreasing to 191k. The four-week moving average of initial jobless claims was down by 250 to 196.25k.

February Jobs Report – BLS Summary – Released 3/10/2023 – The US Economy added 311k nonfarm jobs in February and the Unemployment rate increased 0.2% to 3.6%. Average hourly earnings increased 8 cents to $33.09. Hiring highlights include +105k Leisure and Hospitality, +74k Education and Health Services, +50k Retail Trade, +46 Government, and +45k Professional and Business Services.

- Average hourly earnings increased 8 cents/0.2% to $33.09.

- U3 unemployment rate increased 0.2% to 3.6%. U6 unemployment rate increased 0.2% to 6.8%.

- The labor force participation rate was little changed at 62.5%.

- Average work week decreased by 0.1 to 34.5 hours.

Job Openings & Labor Turnover Survey JOLTS – Released 3/8/2023 – The number of job openings decreased to 10.8 million on the last business day of January, the U.S. Bureau of Labor Statistics reported. Over the month the number of hires and total separations changed little at 6.4 million and 5.9 million, respectively. Within separations, quits (3.9 million) and layoffs and discharges (1.7 million) increased.

Employment Cost Index – Released 1/31/2023 – Compensation costs for civilian workers increased 1.0% for the 3-month period ending in December 2022. The 12-month period ending on December 2022 saw compensation costs increase by 5.1%. The 12-month period ending December 2021 increased 4.0%. Wages and salaries increased 5.1 percent over the year and increased 4.5 percent for the 12-month period ending in December 2021. Benefit costs increased 4.9 percent over the year and increased 2.8 percent for the 12-month period ending in December 2021. This report is published quarterly.

This Week’s Economic Data

Links take you to the data source

Durable Goods – Released 3/24/2023 – New orders for manufactured durable goods in February decreased $2.6 billion or 1.0% to $268.4 billion. Transportation equipment led the decrease down $2.6 billion or 2.8% to $89.4 billion.

New Residential Sales – Released 3/23/2023 – Sales of new single-family homes increased 1.1% to 640k, seasonally adjusted, in February. The median sales price of new homes sold in February was $438,200 with an average sales price of $498,700. At the end of February, the seasonally adjusted estimate of new homes for sale was 436k. This represents a supply of 8.2 months at the current sales rate.

Existing Home Sales – Released 3/21/2023 – Existing home sales increased in February following twelve consecutive months of declines. Sales increased 14.5% to a seasonally adjusted rate of 4.58 million in February. Sales decreased 22.6% year-over-year. Housing inventory sits at 980k units. Identical to January’s inventory. Up 15.3% over last year. Unsold inventory sits at a 2.6-month supply. The median existing home price for all housing types was $363,000 which is down 0.2% from February 2022. February ended 131 consecutive months of year-over-year increases, the longest-running streak on record.

Recent Economic Date

Links take you to the data source

Industrial Production and Capacity Utilization – Released 3/17/2023 – In February Industrial production was unchanged. Manufacturing increased 0.1%. Utilities output increased 0.5%. Mining output declined 0.6%. Total industrial production was 0.2% lower in February than a year ago. Total capacity utilization was unchanged in February at 78.0% which is 1.6% below its long run average.

Housing Starts – Released 3/16/2023 – New home starts in February were at a seasonally adjusted annual rate of 1.450 million; up 9.8% above January, but 18.4% below last February’s rate. Building Permits were at a seasonally adjusted annual rate of 1.524 million, up 13.8% compared to January, but down 17.9% over last year.

Producer Price Index – Released 3/15/2023 – The PPI for final demand decreased 0.1 percent in February, seasonally adjusted, the U.S. Bureau of Labor Statistics reported. Final demand prices increased 0.3 percent in January but decreased 0.2 percent in December. On an unadjusted basis, the index for final demand increased 4.6 percent year over year.

Retail Sales – Released 3/15/2023 – U.S. retail sales for February decreased 0.4% to $697.9 billion but retail sales are 5.4% above February 2022. U.S. retail sales for the December 2022 through February 2023 period were up 6.4% from the same period a year ago.

Consumer Price Index – Released 3/14/2023 – Consumer prices increased 0.4% m/m in February following a 0.5% increase in January. Consumer prices are up 6.0% for the 12-month period ending in February. Core consumer prices increased 0.5% m/m in February.

U.S. Trade Balance – Released 3/8/2023 – The U.S. monthly international trade deficit increased in January 2023 according to the U.S. Bureau of Economic Analysis and the U.S. Census Bureau. The deficit increased from $67.2 billion in December (revised) to $68.3 billion in January. January exports were $257.5 billion, $8.5 billion more than December exports. January imports were $325.8 billion, $9.6 billion more than December imports. Year-over-year, the goods and services deficit decreased $19.2 billion, or 21.9 percent, from January 2022. Exports increased $30.2 billion or 13.3 percent. Imports increased $11.0 billion or 3.5 percent.

Consumer Credit – Released 3/7/2023 – In January, consumer credit increased at a seasonally adjusted annual rate of 3.7 percent. Revolving credit increased at an annual rate of 11.1 percent, while nonrevolving credit increased at an annual rate of 1.2 percent.

US Light Vehicle Sales – Released 3/3/2023 – U.S. light vehicle sales were at a seasonally adjusted annual rate (SAAR) of 14.886 million units in February.

PMI Non-Manufacturing Index – Released 3/3/2023 – Economic activity fell in February. The Services PMI® registered 55.1 percent, 0.1 percentage points lower than January. In January the Services PMI® registered 55.2 percent.

PMI Manufacturing Index – Released 3/1/2023 – The February Manufacturing PMI® registered 47.7 percent, 0.3 percentage point higher than the 47.4 percent recorded in January. Regarding the overall economy, this figure indicates three months of contraction following 30 months of expansion. The New Orders Index remained in contraction territory at 47.0 percent, 4.5 percentage points higher than the 42.5 percent recorded in January. The production index declined 0.7 percentage points to 47.3.

U.S. Construction Spending – Released 3/1/2023 – Construction spending during January 2023 was estimated at a seasonally adjusted annual rate of $1,825.7 billion, 0.1 percent below the revised December estimate of $1,827.5 billion. The January figure is 5.7 percent above the January 2022 estimate of $1,726.6 billion.

Chicago PMI – Released 2/28/2023 – Chicago PMI remained in contraction territory and decreased in February to 43.6 points down from 44.3 points in January. This is the lowest reading since November 2022 and marks six consecutive months in contractionary territory.

Consumer Confidence – Released 2/28/2023 – The Conference Board Consumer Confidence Index® decreased in February. The Index now stands at 102.9 (1985=100), down from 106.0 in January.

Personal Income – Released 2/24/2023 – Personal income increased $131.1 billion, or 0.6 percent in January. Disposable Personal Income increased $387.4 billion or 2.0 percent. Personal Consumption Expenditure increased $312.5 billion or 1.8 percent.

Second Estimate of 4th Quarter 2022 GDP – Released 2/23/2023 – Real gross domestic product (GDP) increased at an annual rate of 2.7 percent in the fourth quarter of 2022 according to the second estimate released by the Bureau of Economic Analysis, following an increase of 3.2 percent in the third quarter of 2022. The advance estimate saw real GDP increase by 2.9%.The GDP estimate released today is based on source data that are more complete than the advance estimate. The increase in real GDP reflected increases in private inventory investment, consumer spending, federal government spending, state and local government spending, and nonresidential fixed investment that were partly offset by decreases in residential fixed investment and exports. Imports, which are a subtraction in the calculation of GDP, decreased. The updated estimates primarily reflected a downward revision to consumer spending that was partly offset by an upward revision to nonresidential fixed investment. Imports, which are a subtraction in the calculation of GDP, were revised up.

Next week we get data on the Third Estimate of 4th Quarter 2022 GDP, Personal Income, Consumer Confidence, and Chicago

Data Sources:

Bureau of Economic Analysis (BEA)

Congressional Budget Office (CBO)

U.S. Bureau of Labor Statistics (BLS)

Federal Reserve Economic Data (FRED Charts)

CME Fed Watch

U.S. Treasury – Yields

U.S. Census Bureau

Institute for Supply Management (ISM)

Weekly DOL Employment Data

BLS Monthly Jobs Report

JOLTS

US Energy Admin (EIA)

BLS Consumer Price Index CPI

BLS Producer Price Index PPI

Atlanta Fed GDPNOW

NY Fed Nowcast GDP

US Census Bureau Housing Starts

Consumer Credit

USCB Retail Sales

Construction Spending

Federal Reserve Dot Plots

NY Empire Index

Philadelphia Federal Reserve

P/E Ratio Data -Yardeni Research

Technical Analysis Info:

StockCharts.com – Financial Charts

Exponential vs Simple moving average

Other Links:

1973 Arab Oil Embargo

Hunt Brothers Silver

Long-Term Capital bailout

Week 12 Talking Points

Table of Contents

Good Life Advisors – Talking Points – Week 12

The 2nd quarter WAM rebalance is coming up Monday, April 3rd. The client-approved model updates and summary outlook will be out tomorrow 3/27. The larger quarterly commentary is coming soon.

Equities ended the week modestly higher despite a very bumpy ride. Most of the focus was on banking sector and the Federal Reserve. Investors are on lookout for any contagion and attempting to gauge the fallout after the FDIC takeover of SVB and Signature two weeks ago. In response, the KBW Bank Index fell for a third-straight week and is now down nearly 29% for the month, on pace for the worst monthly performance since January 2009. Outside the states, UBS agreed to take over its longtime Swiss rival Credit Suisse for a paltry $3 billion. This led to some stabilization initially, but there are still major worries about Deutsche Bank, Germany’s largest.

The March FOMC meeting ended with a unanimous 25 bp rate hike. Headed into the meeting, markets expected a ~90% chance of a 25 bp hike, with a 10% chance for a pause. However, the policy statement changed the language around future increases, which now reads “some additional policy firming may be appropriate.” The updated Summary of Economic Projections also showed the 2023 median dot of 5.1%, unchanged from the December projection. There were also no changes to the balance sheet runoff as some previews suggested. In the post-meeting press conference, Chair Powell said credit tightening could have the same impact as Fed policy, though some economists cautioned of upside risk to the policy path if bank stresses subside. Powell also played down rate cuts, saying Fed officials generally don’t expect rate cuts this year. While markets sold off following the meeting on rate cut pushback (and Treasury Secretary’s simultaneous commentary pushing back against blanket deposit guarantees), a Thursday rally was tabbed to what some economists said was a dovish hike. Markets see the current fed funds rate as the peak and expect between 100 and 125 bp of rate cuts by year-end.

There was mixed messaging around deposit guarantees and FDIC insurance as Treasury Secretary Yellen said she has not considered blanket insurance for US banking deposits without approval from Congress. These comments diverged from Fed Chair Powell, who was speaking simultaneously and said that depositors should assume that their deposits are safe (though Yellen changed her opening statement on Thursday’s hearing to say Treasury is prepared to take additional actions if warranted). However, a blanket guarantee would fall on Congress and not Treasury, though Bloomberg noted this week Senate Banking Chair Brown said prospects around lifting the FDIC cap are improving. The Senate Banking Committee is set to hold hearings on the collapse of SVB and Signature Bank this coming week.

There was a big focus this week on the rally across tech. The Goldman Sachs trading desk highlighted the continued MF rotation out of cyclicals and into supercap tech (where they have been underweight for an extended period of time), and noted that Nasdaq has now outperformed the equal-weight S&P by >10pts in March, the second biggest monthly spread in ~20 years. A number of press articles highlighted the FOMO around a Fed pivot, with managers not wanting to lose out on potential returns if the market rallies. However, central bank tightening remains a key risk with major central banks continuing to push ahead with rate hikes despite tighter financial conditions and bank turmoil. There are also growing concerns around commercial real estate. FT noted CRE loans make up 43% of small bank total lending vs 13% for the biggest banks, putting further scrutiny on regional banks.

Fixed Income

Yield Curve

The current banking situation may have been the catalyst for 10 minus two inversion to start its way back to a positive spread.

January FOMC Statement January Fed Minutes Balance Sheet Reduction Plan Credit, Liquidity and Balance Sheet Federal Reserve Dot Plots

Treasury.gov yields FOMC Policy Normalization Statement Longer- Run Goals Jan 2022

Foreign Exchange Market

Energy Complex

The Baker Hughes rig count was up by 4 this week. There are 758 oil and gas rigs operating in the US – Up 88 over last year.

Metals Complex

Employment Picture

Weekly Unemployment Claims – Released Thursday 3/23/2023 – The week ending March 18th observed a decrease of 1k in initial claims decreasing to 191k. The four-week moving average of initial jobless claims was down by 250 to 196.25k.

February Jobs Report – BLS Summary – Released 3/10/2023 – The US Economy added 311k nonfarm jobs in February and the Unemployment rate increased 0.2% to 3.6%. Average hourly earnings increased 8 cents to $33.09. Hiring highlights include +105k Leisure and Hospitality, +74k Education and Health Services, +50k Retail Trade, +46 Government, and +45k Professional and Business Services.

Job Openings & Labor Turnover Survey JOLTS – Released 3/8/2023 – The number of job openings decreased to 10.8 million on the last business day of January, the U.S. Bureau of Labor Statistics reported. Over the month the number of hires and total separations changed little at 6.4 million and 5.9 million, respectively. Within separations, quits (3.9 million) and layoffs and discharges (1.7 million) increased.

Employment Cost Index – Released 1/31/2023 – Compensation costs for civilian workers increased 1.0% for the 3-month period ending in December 2022. The 12-month period ending on December 2022 saw compensation costs increase by 5.1%. The 12-month period ending December 2021 increased 4.0%. Wages and salaries increased 5.1 percent over the year and increased 4.5 percent for the 12-month period ending in December 2021. Benefit costs increased 4.9 percent over the year and increased 2.8 percent for the 12-month period ending in December 2021. This report is published quarterly.

This Week’s Economic Data

Links take you to the data source

Durable Goods – Released 3/24/2023 – New orders for manufactured durable goods in February decreased $2.6 billion or 1.0% to $268.4 billion. Transportation equipment led the decrease down $2.6 billion or 2.8% to $89.4 billion.

New Residential Sales – Released 3/23/2023 – Sales of new single-family homes increased 1.1% to 640k, seasonally adjusted, in February. The median sales price of new homes sold in February was $438,200 with an average sales price of $498,700. At the end of February, the seasonally adjusted estimate of new homes for sale was 436k. This represents a supply of 8.2 months at the current sales rate.

Existing Home Sales – Released 3/21/2023 – Existing home sales increased in February following twelve consecutive months of declines. Sales increased 14.5% to a seasonally adjusted rate of 4.58 million in February. Sales decreased 22.6% year-over-year. Housing inventory sits at 980k units. Identical to January’s inventory. Up 15.3% over last year. Unsold inventory sits at a 2.6-month supply. The median existing home price for all housing types was $363,000 which is down 0.2% from February 2022. February ended 131 consecutive months of year-over-year increases, the longest-running streak on record.

Recent Economic Date

Links take you to the data source

Industrial Production and Capacity Utilization – Released 3/17/2023 – In February Industrial production was unchanged. Manufacturing increased 0.1%. Utilities output increased 0.5%. Mining output declined 0.6%. Total industrial production was 0.2% lower in February than a year ago. Total capacity utilization was unchanged in February at 78.0% which is 1.6% below its long run average.

Housing Starts – Released 3/16/2023 – New home starts in February were at a seasonally adjusted annual rate of 1.450 million; up 9.8% above January, but 18.4% below last February’s rate. Building Permits were at a seasonally adjusted annual rate of 1.524 million, up 13.8% compared to January, but down 17.9% over last year.

Producer Price Index – Released 3/15/2023 – The PPI for final demand decreased 0.1 percent in February, seasonally adjusted, the U.S. Bureau of Labor Statistics reported. Final demand prices increased 0.3 percent in January but decreased 0.2 percent in December. On an unadjusted basis, the index for final demand increased 4.6 percent year over year.

Retail Sales – Released 3/15/2023 – U.S. retail sales for February decreased 0.4% to $697.9 billion but retail sales are 5.4% above February 2022. U.S. retail sales for the December 2022 through February 2023 period were up 6.4% from the same period a year ago.

Consumer Price Index – Released 3/14/2023 – Consumer prices increased 0.4% m/m in February following a 0.5% increase in January. Consumer prices are up 6.0% for the 12-month period ending in February. Core consumer prices increased 0.5% m/m in February.

U.S. Trade Balance – Released 3/8/2023 – The U.S. monthly international trade deficit increased in January 2023 according to the U.S. Bureau of Economic Analysis and the U.S. Census Bureau. The deficit increased from $67.2 billion in December (revised) to $68.3 billion in January. January exports were $257.5 billion, $8.5 billion more than December exports. January imports were $325.8 billion, $9.6 billion more than December imports. Year-over-year, the goods and services deficit decreased $19.2 billion, or 21.9 percent, from January 2022. Exports increased $30.2 billion or 13.3 percent. Imports increased $11.0 billion or 3.5 percent.

Consumer Credit – Released 3/7/2023 – In January, consumer credit increased at a seasonally adjusted annual rate of 3.7 percent. Revolving credit increased at an annual rate of 11.1 percent, while nonrevolving credit increased at an annual rate of 1.2 percent.

US Light Vehicle Sales – Released 3/3/2023 – U.S. light vehicle sales were at a seasonally adjusted annual rate (SAAR) of 14.886 million units in February.

PMI Non-Manufacturing Index – Released 3/3/2023 – Economic activity fell in February. The Services PMI® registered 55.1 percent, 0.1 percentage points lower than January. In January the Services PMI® registered 55.2 percent.

PMI Manufacturing Index – Released 3/1/2023 – The February Manufacturing PMI® registered 47.7 percent, 0.3 percentage point higher than the 47.4 percent recorded in January. Regarding the overall economy, this figure indicates three months of contraction following 30 months of expansion. The New Orders Index remained in contraction territory at 47.0 percent, 4.5 percentage points higher than the 42.5 percent recorded in January. The production index declined 0.7 percentage points to 47.3.

U.S. Construction Spending – Released 3/1/2023 – Construction spending during January 2023 was estimated at a seasonally adjusted annual rate of $1,825.7 billion, 0.1 percent below the revised December estimate of $1,827.5 billion. The January figure is 5.7 percent above the January 2022 estimate of $1,726.6 billion.

Chicago PMI – Released 2/28/2023 – Chicago PMI remained in contraction territory and decreased in February to 43.6 points down from 44.3 points in January. This is the lowest reading since November 2022 and marks six consecutive months in contractionary territory.

Consumer Confidence – Released 2/28/2023 – The Conference Board Consumer Confidence Index® decreased in February. The Index now stands at 102.9 (1985=100), down from 106.0 in January.

Personal Income – Released 2/24/2023 – Personal income increased $131.1 billion, or 0.6 percent in January. Disposable Personal Income increased $387.4 billion or 2.0 percent. Personal Consumption Expenditure increased $312.5 billion or 1.8 percent.

Second Estimate of 4th Quarter 2022 GDP – Released 2/23/2023 – Real gross domestic product (GDP) increased at an annual rate of 2.7 percent in the fourth quarter of 2022 according to the second estimate released by the Bureau of Economic Analysis, following an increase of 3.2 percent in the third quarter of 2022. The advance estimate saw real GDP increase by 2.9%.The GDP estimate released today is based on source data that are more complete than the advance estimate. The increase in real GDP reflected increases in private inventory investment, consumer spending, federal government spending, state and local government spending, and nonresidential fixed investment that were partly offset by decreases in residential fixed investment and exports. Imports, which are a subtraction in the calculation of GDP, decreased. The updated estimates primarily reflected a downward revision to consumer spending that was partly offset by an upward revision to nonresidential fixed investment. Imports, which are a subtraction in the calculation of GDP, were revised up.

Next week we get data on the Third Estimate of 4th Quarter 2022 GDP, Personal Income, Consumer Confidence, and Chicago

Data Sources:

Bureau of Economic Analysis (BEA)

Congressional Budget Office (CBO)

U.S. Bureau of Labor Statistics (BLS)

Federal Reserve Economic Data (FRED Charts)

CME Fed Watch

U.S. Treasury – Yields

U.S. Census Bureau

Institute for Supply Management (ISM)

Weekly DOL Employment Data

BLS Monthly Jobs Report

JOLTS

US Energy Admin (EIA)

BLS Consumer Price Index CPI

BLS Producer Price Index PPI

Atlanta Fed GDPNOW

NY Fed Nowcast GDP

US Census Bureau Housing Starts

Consumer Credit

USCB Retail Sales

Construction Spending

Federal Reserve Dot Plots

NY Empire Index

Philadelphia Federal Reserve

P/E Ratio Data -Yardeni Research

Technical Analysis Info:

StockCharts.com – Financial Charts

Exponential vs Simple moving average

Other Links:

1973 Arab Oil Embargo

Hunt Brothers Silver

Long-Term Capital bailout

Categories:

Tags: