Good Life Advisors – Talking Points – Week 9

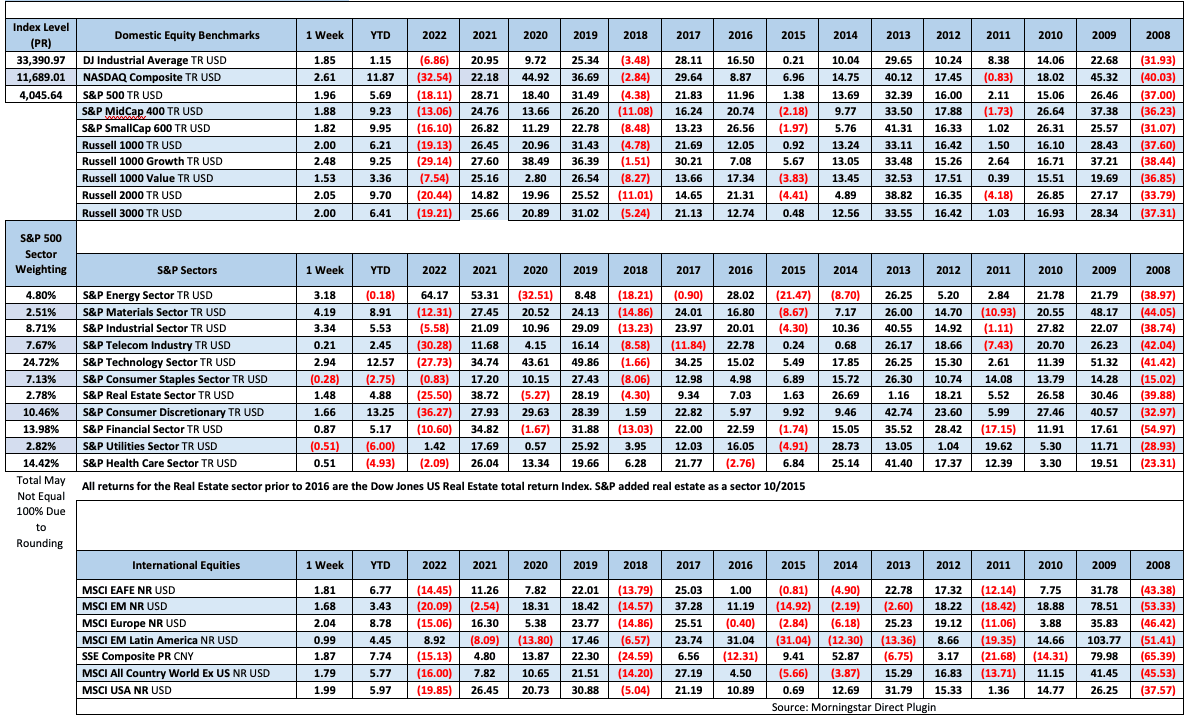

US equities were higher this week, with the S&P rising after three weeks of declines and ending back above the 4000 mark. Treasuries were mostly weaker with the curve flattening. The 2Y yield moved as high as 4.97% on Thursday, and the 10Y and 30Y both spent time above 4%. For anyone interested, both he Six month and one year treasury are yielding over 5% currently. Gold was firmer, rising 2.1% and breaking a four-week streak of declines. Oil was higher; WTI rose 4.4% after two weeks of declines, shaking offsome Friday-morning headlines about tensions within OPEC.

It was a fairly uneventful week for the market as investors kept their focus forward on major catalysts to come, including February nonfarm payrolls (10-Mar) and February CPI (14-Mar). These are expected to help inform both the Fed’s rate trajectory (with the FOMC next meeting on 21-22 March) and the prospects for soft-landing/no-landing economic scenarios.

This week saw a continuation of those debates, particularly the repricing of Fed rate expectations. Ongoing positive surprise momentum in the economic data (and hints of continued inflationary pressures in the February ISM manufacturing report) pushed market expectations for the Fed’s terminal rate above 5.5% at one point, with Fed Governor Waller endorsing a higher peak rate should positive surprises continue. But in a more dovish vein, Atlanta Fed President Bostic said he remains firmly in favor of a 25bp move in March. By week’s end, a 25bp March was still the consensus, but market pricing now does not expect a pivot lower until March 2024.

In the end, the market narrative remained little changed this week, with the path of least resistance still at least somewhat to the downside (though equity-market resilience in the face of Fed-rate repricing continues to be discussed). The upside limit to monetary policy remains something of a moving target, raising worries about growth prospects. But to the bullish side, economic releases and corporate commentary continue to point to a soft- or no-landing scenario, and the market is eagerly anticipating the Fed stepping to the sidelines in the coming months. Straddling these arguments, multiple analysts have voiced skepticism of late that stocks will be able to credibly bounce before seeing some rate reprieve.

Over the weekend, China announced 5.0% GDP target for 2023, at lower end of expectations and below 5.5% prior. Goldman Sachs suggested stronger China PMIs and growth may support Europe vs. US. Comes as markets now discount 4% terminal ECB deposit rate and EZ 5y5y inflation swaps may soon exceed US. Still, broker noted EU equity risk premium not excessively low and may cushion equities from higher yields, providing growth remains resilient. ECB President Lagarde over the weekend said headline inflation to slow in 2023 while core inflation seen stickier. Lagarde’s speech at WTO event this week may be influential. However, investor focus will remain on Fed Chair Powell’s testimony before congress as markets will be looking for clues regarding Fed expectations. US non-farm payrolls another major event as markets try to gauge when the Fed will end the tightening cycle and at what rate.

Fixed Income

Yield Curve

January FOMC Statement January Fed Minutes Balance Sheet Reduction Plan Credit, Liquidity and Balance Sheet Federal Reserve Dot Plots

Treasury.gov yields FOMC Policy Normalization Statement Longer- Run Goals Jan 2022

Foreign Exchange Market

Energy Complex

The Baker Hughes rig count was down by 4 this week. There are 749 oil and gas rigs operating in the US – Up 99 over last year.

Metals Complex

Employment Picture

Weekly Unemployment Claims – Released Thursday 3/2/2023 – The week ending February 25th observed a decrease of 2k in initial claims decreasing to 190k. The four-week moving average of initial jobless claims was up by 1.75k to 193k.

January Jobs Report – BLS Summary – Released 2/3/2023 – The US Economy added 517k nonfarm jobs in January and the Unemployment rate declined to 3.4%. Average hourly earnings increased 10 cents to $33.03. Hiring highlights include +128k Leisure and Hospitality, +105k Education and Health Services, and +82 Professional and Business Services.

- Average hourly earnings increased 10 cents/0.3% to $33.03.

- U3 unemployment rate declined 0.1% to 3.4%. U6 unemployment rate increased 0.1% to 6.6%.

- The labor force participation rate was little changed at 62.4%.

- Average work week increased by 0.3 to 34.7 hours.

Job Openings & Labor Turnover Survey JOLTS – Released 2/1/2023 – The number of job openings increased to 11.0 million on the last business day of December, the U.S. Bureau of Labor Statistics reported. Over the month the number of hires and total separations changed little at 6.2 million and 5.9 million, respectively. Within separations, quits (4.1 million) and layoffs and discharges (1.5 million) changed little.

Employment Cost Index – Released 1/31/2023 – Compensation costs for civilian workers increased 1.0% for the 3-month period ending in December 2022. The 12-month period ending on December 2022 saw compensation costs increase by 5.1%. The 12-month period ending December 2021 increased 4.0%. Wages and salaries increased 5.1 percent over the year and increased 4.5 percent for the 12-month period ending in December 2021. Benefit costs increased 4.9 percent over the year and increased 2.8 percent for the 12-month period ending in December 2021. This report is published quarterly.

This Week’s Economic Data

Links take you to the data source

PMI Non-Manufacturing Index – Released 3/3/2023 – Economic activity fell in February. The Services PMI® registered 55.1 percent, 0.1 percentage points lower than January. In January the Services PMI® registered 55.2 percent.

PMI Manufacturing Index – Released 3/1/2023 – The February Manufacturing PMI® registered 47.7 percent, 0.3 percentage point higher than the 47.4 percent recorded in January. Regarding the overall economy, this figure indicates three months of contraction following 30 months of expansion. The New Orders Index remained in contraction territory at 47.0 percent, 4.5 percentage points higher than the 42.5 percent recorded in January. The production index declined 0.7 percentage points to 47.3.

U.S. Construction Spending– Released 3/1/2023 – Construction spending during January 2023 was estimated at a seasonally adjusted annual rate of $1,825.7 billion, 0.1 percent below the revised December estimate of $1,827.5 billion. The January figure is 5.7 percent above the January 2022 estimate of $1,726.6 billion.

Chicago PMI– Released 2/28/2023 – Chicago PMI remained in contraction territory and decreased in February to 43.6 points down from 44.3 points in January. This is the lowest reading since November 2022 and marks six consecutive months in contractionary territory.

Consumer Confidence– Released 2/28/2023 – The Conference Board Consumer Confidence Index® decreased in February. The Index now stands at 102.9 (1985=100), down from 106.0 in January.

Durable Goods Released 2/27/2023 – New orders for manufactured durable goods in January decreased $13.0 billion or 4.5% to $272.3 billion. Transportation equipment led the decrease down $14.2 billion or 13.3% to $92.8 billion.

Recent Economic Date

Links take you to the data source

Personal Income – Released 2/24/2023 – Personal income increased $131.1 billion, or 0.6 percent in January. Disposable Personal Income increased $387.4 billion or 2.0 percent. Personal Consumption Expenditure increased $312.5 billion or 1.8 percent.

New Residential Sales Released 2/24/2023 – Sales of new single-family homes increased 7.2% to 670k, seasonally adjusted, in January. The median sales price of new homes sold in January was $427,500 with an average sales price of $474,400. At the end of January, the seasonally adjusted estimate of new homes for sale was 439k. This represents a supply of 7.9 months at the current sales rate.

Second Estimate of 4th Quarter 2022 GDP Released 2/23/2023 – Real gross domestic product (GDP) increased at an annual rate of 2.7 percent in the fourth quarter of 2022 according to the second estimate released by the Bureau of Economic Analysis, following an increase of 3.2 percent in the third quarter of 2022. The advance estimate saw real GDP increase by 2.9%.The GDP estimate released today is based on source data that are more complete than the advance estimate. The increase in real GDP reflected increases in private inventory investment, consumer spending, federal government spending, state and local government spending, and nonresidential fixed investment that were partly offset by decreases in residential fixed investment and exports. Imports, which are a subtraction in the calculation of GDP, decreased. The updated estimates primarily reflected a downward revision to consumer spending that was partly offset by an upward revision to nonresidential fixed investment. Imports, which are a subtraction in the calculation of GDP, were revised up.

Existing Home Sales Released 2/21/2023 – Existing home sales decreased in January marking twelve consecutive months of declines. Sales declined 0.7% to a seasonally adjusted rate of 4.0 million in January. Sales decreased 36.9% year-over-year. Housing inventory sits at 980k units. Up 2.1% from December’s inventory. Up 15.3% over last year. Unsold inventory sits at a 2.9-month supply. The median existing home price for all housing types was $359,000 which is up 1.3% from January 2021. This marks 131 consecutive months of year-over-year increases, the longest-running streak on record.

Producer Price Index – Released 2/16/2023 – The PPI for final demand increased 0.7 percent in January, seasonally adjusted, the U.S. Bureau of Labor Statistics reported. Final demand prices declined 0.2 percent in December but increased 0.3 percent in November. On an unadjusted basis, the index for final demand increased 6.0 percent year over year.

Housing Starts– Released 2/16/2023 – New home starts in January were at a seasonally adjusted annual rate of 1.309 million; down 4.5% below December, and 21.4% below last January’s rate. Building Permits were at a seasonally adjusted annual rate of 1.339 million, up 0.1% compared to December, but down 27.3% over last year.

Industrial Production and Capacity Utilization Released 2/15/2023 – In January Industrial production was unchanged. Manufacturing increased 1.0%. Utilities output decreased 9.9%. Mining output increased 2.0%. Total industrial production was 0.8% higher in January than a year ago. Total capacity utilization decreased 0.1% in January to 78.3% which is 1.3% below its long run average.

Retail Sales– Released 2/15/2023 – U.S. retail sales for January increased 3.0% to $697.0 billion and retail sales are 6.4% above January 2022. U.S. retail sales for the November 2022 through January 2023 period were up 6.1% from the same period a year ago.

Consumer Price Index – Released 2/14/2023 – Consumer prices increased 0.5% m/m in January following a 0.1% increase in December. Consumer prices are up 6.4% for the 12-month period ending in January. Core consumer prices increased 0.4% m/m in January.

Consumer Credit – Released 2/7/2023 – In December, consumer credit increased at a seasonally adjusted annual rate of 7.8 percent. Revolving credit increased at an annual rate of 14.8 percent, while nonrevolving credit increased at an annual rate of 5.6 percent.

U.S. Trade Balance – Released 2/7/2023 – The U.S. monthly international trade deficit increased in December 2022 according to the U.S. Bureau of Economic Analysis and the U.S. Census Bureau. The deficit increased from $61.0 billion in November (revised) to $67.4 billion in December. December exports were $250.2 billion, $2.2 billion less than November exports. December imports were $317.6 billion, $4.2 billion more than November imports. In 2022, the goods and services deficit increased $103.0 billion, or 12.2 percent, from 2021. Exports increased $453.1 billion or 17.7 percent. Imports increased $556.1 billion or 16.3 percent.

US Light Vehicle Sales– Released 2/3/2023 – U.S. light vehicle sales were at a seasonally adjusted annual rate (SAAR) of 15.738 million units in January.

Next week we get data on U.S. Trade Balance, Consumer Credit, JOLTS, and the February Jobs Report.

Data Sources:

Bureau of Economic Analysis (BEA)

Congressional Budget Office (CBO)

U.S. Bureau of Labor Statistics (BLS)

Federal Reserve Economic Data (FRED Charts)

CME Fed Watch

U.S. Treasury – Yields

U.S. Census Bureau

Institute for Supply Management (ISM)

Weekly DOL Employment Data

BLS Monthly Jobs Report

JOLTS

US Energy Admin (EIA)

BLS Consumer Price Index CPI

BLS Producer Price Index PPI

Atlanta Fed GDPNOW

NY Fed Nowcast GDP

US Census Bureau Housing Starts

Consumer Credit

USCB Retail Sales

Construction Spending

Federal Reserve Dot Plots

NY Empire Index

Philadelphia Federal Reserve

P/E Ratio Data -Yardeni Research

Technical Analysis Info:

StockCharts.com – Financial Charts

Exponential vs Simple moving average

Other Links:

1973 Arab Oil Embargo

Hunt Brothers Silver

Long-Term Capital bailout

Week 9 Talking Points

Table of Contents

Good Life Advisors – Talking Points – Week 9

US equities were higher this week, with the S&P rising after three weeks of declines and ending back above the 4000 mark. Treasuries were mostly weaker with the curve flattening. The 2Y yield moved as high as 4.97% on Thursday, and the 10Y and 30Y both spent time above 4%. For anyone interested, both he Six month and one year treasury are yielding over 5% currently. Gold was firmer, rising 2.1% and breaking a four-week streak of declines. Oil was higher; WTI rose 4.4% after two weeks of declines, shaking offsome Friday-morning headlines about tensions within OPEC.

It was a fairly uneventful week for the market as investors kept their focus forward on major catalysts to come, including February nonfarm payrolls (10-Mar) and February CPI (14-Mar). These are expected to help inform both the Fed’s rate trajectory (with the FOMC next meeting on 21-22 March) and the prospects for soft-landing/no-landing economic scenarios.

This week saw a continuation of those debates, particularly the repricing of Fed rate expectations. Ongoing positive surprise momentum in the economic data (and hints of continued inflationary pressures in the February ISM manufacturing report) pushed market expectations for the Fed’s terminal rate above 5.5% at one point, with Fed Governor Waller endorsing a higher peak rate should positive surprises continue. But in a more dovish vein, Atlanta Fed President Bostic said he remains firmly in favor of a 25bp move in March. By week’s end, a 25bp March was still the consensus, but market pricing now does not expect a pivot lower until March 2024.

In the end, the market narrative remained little changed this week, with the path of least resistance still at least somewhat to the downside (though equity-market resilience in the face of Fed-rate repricing continues to be discussed). The upside limit to monetary policy remains something of a moving target, raising worries about growth prospects. But to the bullish side, economic releases and corporate commentary continue to point to a soft- or no-landing scenario, and the market is eagerly anticipating the Fed stepping to the sidelines in the coming months. Straddling these arguments, multiple analysts have voiced skepticism of late that stocks will be able to credibly bounce before seeing some rate reprieve.

Over the weekend, China announced 5.0% GDP target for 2023, at lower end of expectations and below 5.5% prior. Goldman Sachs suggested stronger China PMIs and growth may support Europe vs. US. Comes as markets now discount 4% terminal ECB deposit rate and EZ 5y5y inflation swaps may soon exceed US. Still, broker noted EU equity risk premium not excessively low and may cushion equities from higher yields, providing growth remains resilient. ECB President Lagarde over the weekend said headline inflation to slow in 2023 while core inflation seen stickier. Lagarde’s speech at WTO event this week may be influential. However, investor focus will remain on Fed Chair Powell’s testimony before congress as markets will be looking for clues regarding Fed expectations. US non-farm payrolls another major event as markets try to gauge when the Fed will end the tightening cycle and at what rate.

Fixed Income

Yield Curve

January FOMC Statement January Fed Minutes Balance Sheet Reduction Plan Credit, Liquidity and Balance Sheet Federal Reserve Dot Plots

Treasury.gov yields FOMC Policy Normalization Statement Longer- Run Goals Jan 2022

Foreign Exchange Market

Energy Complex

The Baker Hughes rig count was down by 4 this week. There are 749 oil and gas rigs operating in the US – Up 99 over last year.

Metals Complex

Employment Picture

Weekly Unemployment Claims – Released Thursday 3/2/2023 – The week ending February 25th observed a decrease of 2k in initial claims decreasing to 190k. The four-week moving average of initial jobless claims was up by 1.75k to 193k.

January Jobs Report – BLS Summary – Released 2/3/2023 – The US Economy added 517k nonfarm jobs in January and the Unemployment rate declined to 3.4%. Average hourly earnings increased 10 cents to $33.03. Hiring highlights include +128k Leisure and Hospitality, +105k Education and Health Services, and +82 Professional and Business Services.

Job Openings & Labor Turnover Survey JOLTS – Released 2/1/2023 – The number of job openings increased to 11.0 million on the last business day of December, the U.S. Bureau of Labor Statistics reported. Over the month the number of hires and total separations changed little at 6.2 million and 5.9 million, respectively. Within separations, quits (4.1 million) and layoffs and discharges (1.5 million) changed little.

Employment Cost Index – Released 1/31/2023 – Compensation costs for civilian workers increased 1.0% for the 3-month period ending in December 2022. The 12-month period ending on December 2022 saw compensation costs increase by 5.1%. The 12-month period ending December 2021 increased 4.0%. Wages and salaries increased 5.1 percent over the year and increased 4.5 percent for the 12-month period ending in December 2021. Benefit costs increased 4.9 percent over the year and increased 2.8 percent for the 12-month period ending in December 2021. This report is published quarterly.

This Week’s Economic Data

Links take you to the data source

PMI Non-Manufacturing Index – Released 3/3/2023 – Economic activity fell in February. The Services PMI® registered 55.1 percent, 0.1 percentage points lower than January. In January the Services PMI® registered 55.2 percent.

PMI Manufacturing Index – Released 3/1/2023 – The February Manufacturing PMI® registered 47.7 percent, 0.3 percentage point higher than the 47.4 percent recorded in January. Regarding the overall economy, this figure indicates three months of contraction following 30 months of expansion. The New Orders Index remained in contraction territory at 47.0 percent, 4.5 percentage points higher than the 42.5 percent recorded in January. The production index declined 0.7 percentage points to 47.3.

U.S. Construction Spending– Released 3/1/2023 – Construction spending during January 2023 was estimated at a seasonally adjusted annual rate of $1,825.7 billion, 0.1 percent below the revised December estimate of $1,827.5 billion. The January figure is 5.7 percent above the January 2022 estimate of $1,726.6 billion.

Chicago PMI– Released 2/28/2023 – Chicago PMI remained in contraction territory and decreased in February to 43.6 points down from 44.3 points in January. This is the lowest reading since November 2022 and marks six consecutive months in contractionary territory.

Consumer Confidence– Released 2/28/2023 – The Conference Board Consumer Confidence Index® decreased in February. The Index now stands at 102.9 (1985=100), down from 106.0 in January.

Durable Goods Released 2/27/2023 – New orders for manufactured durable goods in January decreased $13.0 billion or 4.5% to $272.3 billion. Transportation equipment led the decrease down $14.2 billion or 13.3% to $92.8 billion.

Recent Economic Date

Links take you to the data source

Personal Income – Released 2/24/2023 – Personal income increased $131.1 billion, or 0.6 percent in January. Disposable Personal Income increased $387.4 billion or 2.0 percent. Personal Consumption Expenditure increased $312.5 billion or 1.8 percent.

New Residential Sales Released 2/24/2023 – Sales of new single-family homes increased 7.2% to 670k, seasonally adjusted, in January. The median sales price of new homes sold in January was $427,500 with an average sales price of $474,400. At the end of January, the seasonally adjusted estimate of new homes for sale was 439k. This represents a supply of 7.9 months at the current sales rate.

Second Estimate of 4th Quarter 2022 GDP Released 2/23/2023 – Real gross domestic product (GDP) increased at an annual rate of 2.7 percent in the fourth quarter of 2022 according to the second estimate released by the Bureau of Economic Analysis, following an increase of 3.2 percent in the third quarter of 2022. The advance estimate saw real GDP increase by 2.9%.The GDP estimate released today is based on source data that are more complete than the advance estimate. The increase in real GDP reflected increases in private inventory investment, consumer spending, federal government spending, state and local government spending, and nonresidential fixed investment that were partly offset by decreases in residential fixed investment and exports. Imports, which are a subtraction in the calculation of GDP, decreased. The updated estimates primarily reflected a downward revision to consumer spending that was partly offset by an upward revision to nonresidential fixed investment. Imports, which are a subtraction in the calculation of GDP, were revised up.

Existing Home Sales Released 2/21/2023 – Existing home sales decreased in January marking twelve consecutive months of declines. Sales declined 0.7% to a seasonally adjusted rate of 4.0 million in January. Sales decreased 36.9% year-over-year. Housing inventory sits at 980k units. Up 2.1% from December’s inventory. Up 15.3% over last year. Unsold inventory sits at a 2.9-month supply. The median existing home price for all housing types was $359,000 which is up 1.3% from January 2021. This marks 131 consecutive months of year-over-year increases, the longest-running streak on record.

Producer Price Index – Released 2/16/2023 – The PPI for final demand increased 0.7 percent in January, seasonally adjusted, the U.S. Bureau of Labor Statistics reported. Final demand prices declined 0.2 percent in December but increased 0.3 percent in November. On an unadjusted basis, the index for final demand increased 6.0 percent year over year.

Housing Starts– Released 2/16/2023 – New home starts in January were at a seasonally adjusted annual rate of 1.309 million; down 4.5% below December, and 21.4% below last January’s rate. Building Permits were at a seasonally adjusted annual rate of 1.339 million, up 0.1% compared to December, but down 27.3% over last year.

Industrial Production and Capacity Utilization Released 2/15/2023 – In January Industrial production was unchanged. Manufacturing increased 1.0%. Utilities output decreased 9.9%. Mining output increased 2.0%. Total industrial production was 0.8% higher in January than a year ago. Total capacity utilization decreased 0.1% in January to 78.3% which is 1.3% below its long run average.

Retail Sales– Released 2/15/2023 – U.S. retail sales for January increased 3.0% to $697.0 billion and retail sales are 6.4% above January 2022. U.S. retail sales for the November 2022 through January 2023 period were up 6.1% from the same period a year ago.

Consumer Price Index – Released 2/14/2023 – Consumer prices increased 0.5% m/m in January following a 0.1% increase in December. Consumer prices are up 6.4% for the 12-month period ending in January. Core consumer prices increased 0.4% m/m in January.

Consumer Credit – Released 2/7/2023 – In December, consumer credit increased at a seasonally adjusted annual rate of 7.8 percent. Revolving credit increased at an annual rate of 14.8 percent, while nonrevolving credit increased at an annual rate of 5.6 percent.

U.S. Trade Balance – Released 2/7/2023 – The U.S. monthly international trade deficit increased in December 2022 according to the U.S. Bureau of Economic Analysis and the U.S. Census Bureau. The deficit increased from $61.0 billion in November (revised) to $67.4 billion in December. December exports were $250.2 billion, $2.2 billion less than November exports. December imports were $317.6 billion, $4.2 billion more than November imports. In 2022, the goods and services deficit increased $103.0 billion, or 12.2 percent, from 2021. Exports increased $453.1 billion or 17.7 percent. Imports increased $556.1 billion or 16.3 percent.

US Light Vehicle Sales– Released 2/3/2023 – U.S. light vehicle sales were at a seasonally adjusted annual rate (SAAR) of 15.738 million units in January.

Next week we get data on U.S. Trade Balance, Consumer Credit, JOLTS, and the February Jobs Report.

Data Sources:

Bureau of Economic Analysis (BEA)

Congressional Budget Office (CBO)

U.S. Bureau of Labor Statistics (BLS)

Federal Reserve Economic Data (FRED Charts)

CME Fed Watch

U.S. Treasury – Yields

U.S. Census Bureau

Institute for Supply Management (ISM)

Weekly DOL Employment Data

BLS Monthly Jobs Report

JOLTS

US Energy Admin (EIA)

BLS Consumer Price Index CPI

BLS Producer Price Index PPI

Atlanta Fed GDPNOW

NY Fed Nowcast GDP

US Census Bureau Housing Starts

Consumer Credit

USCB Retail Sales

Construction Spending

Federal Reserve Dot Plots

NY Empire Index

Philadelphia Federal Reserve

P/E Ratio Data -Yardeni Research

Technical Analysis Info:

StockCharts.com – Financial Charts

Exponential vs Simple moving average

Other Links:

1973 Arab Oil Embargo

Hunt Brothers Silver

Long-Term Capital bailout

Categories:

Tags: