Good Life Advisors – Talking Points – Week 17

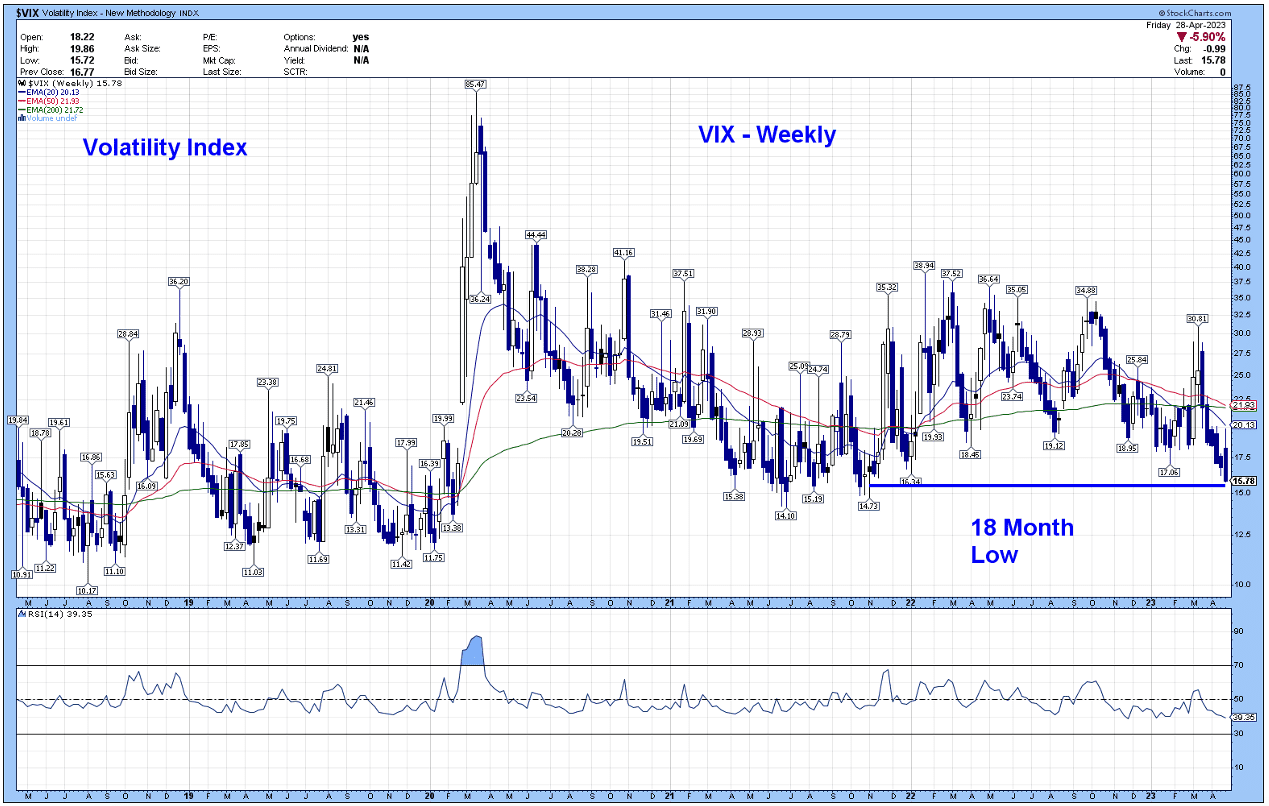

US equities were mostly higher this week, with the Dow, S&P, and Nasdaq shaking off last week’s modest declines. Corporate earnings were a major driver of the market narrative, with 180 S&P 500 constituents reporting this week. Treasuries were stronger across the curve, with the 2Y yield dropping as low as 3.85% at midweek before finishing the week just above 4%. The dollar was weaker on the euro and sterling crosses but outperformed the yen in the wake of this week’s BoJ meeting. Gold was slightly stronger, finishing up 0.4%. WTI crude settled down 1.4%, its second consecutive weekly drop, amid bubbling concerns about the global demand trajectory.

Tech and communication services were the clear sector leaders this week on well-received earnings from META +12.9% and MSFT +7.5%. Media and telecom stocks were mixed, but the groups were boosted by CMCSA +9.6% and VZ +4.1% on their reports. Restaurants, managed care, hospitals, food, HPCs, and homebuilders were among the other outperforming areas. To the downside, banks were mostly lower, particularly the larger caps. There were some notable earnings-linked decliners in parcels/logistics and paper/packaging. Transports, industrial metals, fertilizers, semis, machinery, and A&D were some of the other underperformers.

The market had been going through an unusually quiet period coming into this week, with the S&P 500 having seen only one trading day with a 1%+ move in either direction for the month of April until a drop on Tuesday and a notable Thursday gain broke the pattern. That said, there were not a lot of major directional drivers at play. Earnings dominated the week’s newsflow, though takeaways were mixed. Solid Q1 reports from Big Tech certainly helped sentiment though they also renewed discussion about narrow market leadership. Some bank reports were better than feared, though the ongoing attempts to save FRC (75.5%) revived some banking sector concerns. Elsewhere, the week’s multiple economic releases continued to reflect a slowing economy. The federal debt ceiling also played a bit of a role in the narrative, though the GOP plan passed this week in the House is only one element in what is likely to be a months-long story.

The week’s economic releases were a mixed bag, but with nothing to shift the narrative of a softening macro backdrop. The first read of Q1 GDP showed a larger-than-expected deceleration to a 1.1% seasonally adjusted annual rate (vs. 2.6% in Q4’22), with a focus on a sharp decrease in private inventory investment. March’s durable-goods report showed strong monthly headline growth, though core capital goods orders were weaker. March consumer confidence was missed on the headline, despite some improvement in the present-situation component and a more optimistic labor-market differential. Reports from the Dallas, Richmond, and Kansas City Feds highlighted an ongoing pattern of regional weakness. March new-home sales were much better than expected, though pending-home sales missed consensus. Finally, the March core PCE price index was little changed m/m, though Q1’s employment cost index was a bit hotter.

The debt-ceiling battle continued to heat up in Washington, with House Speaker McCarthy engineering the narrow passage of the GOP’s proposal this week, which calls for raising the debt limit into 2024 in exchange for ~$4.5T in spending concessions. While this generated a lot of headline noise this week, it should be remembered it has no chance of passage in its current form and may be more important as a prod to get Democrats to the negotiating table. This Republican effort came as worries mounted that weak federal tax receipts could pull the “X-date” of potential default into early June. However, analysts increasingly believe the government will have enough resources to pay its obligations through the 15-Jun quarterly estimated-tax deadline, allowing Treasury’s “extraordinary measures” to continue into at least July.

It was a massive week of corporate earnings, featuring reports from 180 S&P 500 constituents (more than 50% of index members have now reported). In general, the season continued to come in better than expected, with FactSet noting that the (3.7%) blended y/y earnings growth rate is better than the (6.7%) expected at the end of Q1 and a notable improvement from last week’s report. Earnings are coming in 6.9% above consensus on average, which is better than nearer-term trends though still lagging the five-year average. There remain no real surprises as to the major themes, including moderating but resilient consumer spending, stabilization/recovery in housing, and ubiquitous corporate cost-cutting/efficiency efforts.

The major macro event next week will be the May FOMC meeting, with its policy statement due out on Wednesday 3-May. The Fed is widely expected to raise rates by 25bp to 4.75-5.00% as well as potentially signal a pause to its hiking campaign. The flood of Q1 earnings reports will continue, with some 162 S&P constituents on next week’s schedule (including AAPL post-close Thursday). Economic releases will include April ISM manufacturing (Monday); March JOLTS job openings (Tuesday); ADP April employment and April’s ISM services report (Wednesday); weekly jobless claims (Thursday); and the April nonfarm payrolls report (Friday). The latter is currently expected to show a gain of 185K jobs, which would be the slowest since December 2020. Finally, the market will be watching for any update out of the Treasury Department about its estimate of when the currently operating “extraordinary measures” will be exhausted; consensus is firming that this may be some time in July.

Fixed Income

Yield Curve

March FOMC Statement March Fed Minutes Balance Sheet Reduction Plan Credit, Liquidity and Balance Sheet Federal Reserve Dot Plots

Treasury.gov yields FOMC Policy Normalization Statement Longer- Run Goals Jan 2022

Foreign Exchange Market

Energy Complex

The Baker Hughes rig count was up by 2 this week. There are 755 oil and gas rigs operating in the US – Up 57 over last year.

Metals Complex

Employment Picture

Weekly Unemployment Claims – Released Thursday 4/20/2023 – The week ending April 15th observed an increase of 5k in initial claims increasing to 245k. The four-week moving average of initial jobless claims was down by 500 to 239.75.

March Jobs Report – BLS Summary – Released 4/7/2023 – The US Economy added 236k nonfarm jobs in March and the Unemployment rate was little changed at 3.5%. Average hourly earnings increased 9 cents to $33.18. Hiring highlights include +72k Leisure and Hospitality, +65k Education and Health Services, +47 Government, and +39k Professional and Business Services.

- Average hourly earnings increased 9 cents/0.3% to $33.18.

- U3 unemployment rate was little changed at 3.5%. U6 unemployment rate decreased 0.1% to 6.7%.

- The labor force participation rate was little changed at 62.6%.

- Average work week decreased by 0.1 to 34.4 hours.

Job Openings & Labor Turnover Survey JOLTS – Released 4/4/2023 – The number of job openings decreased to 9.9 million on the last business day of February, the U.S. Bureau of Labor Statistics reported. Over the month, the number of hires and total separations changed little at 6.2 million and 5.8 million, respectively. Within separations, quits (4.0 million) increased, and layoffs and discharges (1.5 million) decreased.

Employment Cost Index – Released 1/31/2023 – Compensation costs for civilian workers increased 1.0% for the 3-month period ending in December 2022. The 12-month period ending on December 2022 saw compensation costs increase by 5.1%. The 12-month period ending December 2021 increased 4.0%. Wages and salaries increased 5.1 percent over the year and increased 4.5 percent for the 12-month period ending in December 2021. Benefit costs increased 4.9 percent over the year and increased 2.8 percent for the 12-month period ending in December 2021. This report is published quarterly.

This Week’s Economic Data

Links take you to the data source

Existing Home Sales – Released 4/20/2023 – Existing home sales decreased in March. Sales decreased 2.4% to a seasonally adjusted rate of 4.44 million in March. Sales decreased 22.0% year-over-year. Housing inventory sits at 980k units. Up 1.0% over February. Up 5.4% over last year. Unsold inventory sits at a 2.6-month supply. The median existing home price for all housing types was $375,700 which is down 0.9% from March 2022.

Housing Starts – Released 4/18/2023 – New home starts in March were at a seasonally adjusted annual rate of 1.420 million; down 0.8% below February, and 17.2% below last March’s rate. Building Permits were at a seasonally adjusted annual rate of 1.413 million, down 8.8% compared to February, and down 24.8% over last year.

Recent Economic Date

Links take you to the data source

Existing Home Sales – Released 4/20/2023 – Existing home sales decreased in March. Sales decreased 2.4% to a seasonally adjusted rate of 4.44 million in March. Sales decreased 22.0% year-over-year. Housing inventory sits at 980k units. Up 1.0% over February. Up 5.4% over last year. Unsold inventory sits at a 2.6-month supply. The median existing home price for all housing types was $375,700 which is down 0.9% from March 2022.

Housing Starts – Released 4/18/2023 – New home starts in March were at a seasonally adjusted annual rate of 1.420 million; down 0.8% below February, and 17.2% below last March’s rate. Building Permits were at a seasonally adjusted annual rate of 1.413 million, down 8.8% compared to February, and down 24.8% over last year.

Industrial Production and Capacity Utilization – Released 4/14/2023 – In March, Industrial production increased 0.4%. Manufacturing decreased 0.5%. Utilities output increased 8.4%. Mining output declined 0.5%. Total industrial production was 0.5% higher in March than a year ago. Total capacity utilization increased in March to 79.8% which is 0.1% above its long run average.

Retail Sales – Released 4/14/2023 – U.S. retail sales for March decreased 1.0% to $691.7 billion but retail sales are 2.9% above March 2022. U.S. retail sales for the January 2022 through March 2023 period were up 5.4% from the same period a year ago.

Producer Price Index – Released 4/13/2023 – The PPI for final demand decreased 0.5 percent in March, seasonally adjusted, the U.S. Bureau of Labor Statistics reported. Final demand prices were unchanged in February and increased 0.4 percent in January. On an unadjusted basis, the index for final demand increased 2.7 percent year over year.

Consumer Price Index – Released 4/12/2023 – Consumer prices increased 0.1% m/m in March following a 0.4% increase in February. Consumer prices are up 5.0% for the 12-month period ending in March. Core consumer prices increased 0.4% m/m in March.

Consumer Credit – Released 4/7/2023 – In February, consumer credit increased at a seasonally adjusted annual rate of 3.8 percent. Revolving credit increased at an annual rate of 5.0 percent, while nonrevolving credit increased at an annual rate of 3.4 percent.

U.S. Trade Balance – Released 4/5/2023 – The U.S. monthly international trade deficit increased in February 2023 according to the U.S. Bureau of Economic Analysis and the U.S. Census Bureau. The deficit increased from $68.7 billion in January (revised) to $70.5 billion in February. February exports were $251.2 billion, $6.9 billion less than January exports. February imports were $321.7 billion, $5.0 billion less than January imports. Year-to-date, the goods and services deficit decreased $35.5 billion, or 20.3 percent, from the same period in 2022. Exports increased $49.5 billion or 10.8 percent. Imports increased $14.0 billion or 2.2 percent.

PMI Non-Manufacturing Index – Released 4/5/2023 – Economic activity remained in expansionary territory in March. The Services PMI® registered 51.2 percent, 3.9 percentage points lower than February. In February, the Services PMI® registered 55.1 percent.

PMI Manufacturing Index – Released 4/3/2023 – The March Manufacturing PMI® registered 46.3 percent, 1.4 percentage point lower than the 47.7 percent recorded in February. Regarding the overall economy, this figure indicates four months of contraction following 30 months of expansion. The New Orders Index remained in contraction territory at 44.3 percent, 2.7 percentage points lower than the 47.0 percent recorded in February. The production index increased 0.5 percentage points to 47.8.

U.S. Construction Spending – Released 4/3/2023 – Construction spending during February 2023 was estimated at a seasonally adjusted annual rate of $1,844.4 billion, 0.1 percent below the revised January estimate of $1,845.4 billion. The February figure is 5.2 percent above the February 2022 estimate of $1,753.1 billion.

Data Sources:

Bureau of Economic Analysis (BEA)

Congressional Budget Office (CBO)

U.S. Bureau of Labor Statistics (BLS)

Federal Reserve Economic Data (FRED Charts)

CME Fed Watch

U.S. Treasury – Yields

U.S. Census Bureau

Institute for Supply Management (ISM)

Weekly DOL Employment Data

BLS Monthly Jobs Report

JOLTS

US Energy Admin (EIA)

BLS Consumer Price Index CPI

BLS Producer Price Index PPI

Atlanta Fed GDPNOW

NY Fed Nowcast GDP

US Census Bureau Housing Starts

Consumer Credit

USCB Retail Sales

Construction Spending

Federal Reserve Dot Plots

NY Empire Index

Philadelphia Federal Reserve

P/E Ratio Data -Yardeni Research

Technical Analysis Info:

StockCharts.com – Financial Charts

Exponential vs Simple moving average

Other Links:

1973 Arab Oil Embargo

Hunt Brothers Silver

Long-Term Capital bailout

Week 17 Talking Points

Table of Contents

Good Life Advisors – Talking Points – Week 17

US equities were mostly higher this week, with the Dow, S&P, and Nasdaq shaking off last week’s modest declines. Corporate earnings were a major driver of the market narrative, with 180 S&P 500 constituents reporting this week. Treasuries were stronger across the curve, with the 2Y yield dropping as low as 3.85% at midweek before finishing the week just above 4%. The dollar was weaker on the euro and sterling crosses but outperformed the yen in the wake of this week’s BoJ meeting. Gold was slightly stronger, finishing up 0.4%. WTI crude settled down 1.4%, its second consecutive weekly drop, amid bubbling concerns about the global demand trajectory.

Tech and communication services were the clear sector leaders this week on well-received earnings from META +12.9% and MSFT +7.5%. Media and telecom stocks were mixed, but the groups were boosted by CMCSA +9.6% and VZ +4.1% on their reports. Restaurants, managed care, hospitals, food, HPCs, and homebuilders were among the other outperforming areas. To the downside, banks were mostly lower, particularly the larger caps. There were some notable earnings-linked decliners in parcels/logistics and paper/packaging. Transports, industrial metals, fertilizers, semis, machinery, and A&D were some of the other underperformers.

The market had been going through an unusually quiet period coming into this week, with the S&P 500 having seen only one trading day with a 1%+ move in either direction for the month of April until a drop on Tuesday and a notable Thursday gain broke the pattern. That said, there were not a lot of major directional drivers at play. Earnings dominated the week’s newsflow, though takeaways were mixed. Solid Q1 reports from Big Tech certainly helped sentiment though they also renewed discussion about narrow market leadership. Some bank reports were better than feared, though the ongoing attempts to save FRC (75.5%) revived some banking sector concerns. Elsewhere, the week’s multiple economic releases continued to reflect a slowing economy. The federal debt ceiling also played a bit of a role in the narrative, though the GOP plan passed this week in the House is only one element in what is likely to be a months-long story.

The week’s economic releases were a mixed bag, but with nothing to shift the narrative of a softening macro backdrop. The first read of Q1 GDP showed a larger-than-expected deceleration to a 1.1% seasonally adjusted annual rate (vs. 2.6% in Q4’22), with a focus on a sharp decrease in private inventory investment. March’s durable-goods report showed strong monthly headline growth, though core capital goods orders were weaker. March consumer confidence was missed on the headline, despite some improvement in the present-situation component and a more optimistic labor-market differential. Reports from the Dallas, Richmond, and Kansas City Feds highlighted an ongoing pattern of regional weakness. March new-home sales were much better than expected, though pending-home sales missed consensus. Finally, the March core PCE price index was little changed m/m, though Q1’s employment cost index was a bit hotter.

The debt-ceiling battle continued to heat up in Washington, with House Speaker McCarthy engineering the narrow passage of the GOP’s proposal this week, which calls for raising the debt limit into 2024 in exchange for ~$4.5T in spending concessions. While this generated a lot of headline noise this week, it should be remembered it has no chance of passage in its current form and may be more important as a prod to get Democrats to the negotiating table. This Republican effort came as worries mounted that weak federal tax receipts could pull the “X-date” of potential default into early June. However, analysts increasingly believe the government will have enough resources to pay its obligations through the 15-Jun quarterly estimated-tax deadline, allowing Treasury’s “extraordinary measures” to continue into at least July.

It was a massive week of corporate earnings, featuring reports from 180 S&P 500 constituents (more than 50% of index members have now reported). In general, the season continued to come in better than expected, with FactSet noting that the (3.7%) blended y/y earnings growth rate is better than the (6.7%) expected at the end of Q1 and a notable improvement from last week’s report. Earnings are coming in 6.9% above consensus on average, which is better than nearer-term trends though still lagging the five-year average. There remain no real surprises as to the major themes, including moderating but resilient consumer spending, stabilization/recovery in housing, and ubiquitous corporate cost-cutting/efficiency efforts.

The major macro event next week will be the May FOMC meeting, with its policy statement due out on Wednesday 3-May. The Fed is widely expected to raise rates by 25bp to 4.75-5.00% as well as potentially signal a pause to its hiking campaign. The flood of Q1 earnings reports will continue, with some 162 S&P constituents on next week’s schedule (including AAPL post-close Thursday). Economic releases will include April ISM manufacturing (Monday); March JOLTS job openings (Tuesday); ADP April employment and April’s ISM services report (Wednesday); weekly jobless claims (Thursday); and the April nonfarm payrolls report (Friday). The latter is currently expected to show a gain of 185K jobs, which would be the slowest since December 2020. Finally, the market will be watching for any update out of the Treasury Department about its estimate of when the currently operating “extraordinary measures” will be exhausted; consensus is firming that this may be some time in July.

Fixed Income

Yield Curve

March FOMC Statement March Fed Minutes Balance Sheet Reduction Plan Credit, Liquidity and Balance Sheet Federal Reserve Dot Plots

Treasury.gov yields FOMC Policy Normalization Statement Longer- Run Goals Jan 2022

Foreign Exchange Market

Energy Complex

The Baker Hughes rig count was up by 2 this week. There are 755 oil and gas rigs operating in the US – Up 57 over last year.

Metals Complex

Employment Picture

Weekly Unemployment Claims – Released Thursday 4/20/2023 – The week ending April 15th observed an increase of 5k in initial claims increasing to 245k. The four-week moving average of initial jobless claims was down by 500 to 239.75.

March Jobs Report – BLS Summary – Released 4/7/2023 – The US Economy added 236k nonfarm jobs in March and the Unemployment rate was little changed at 3.5%. Average hourly earnings increased 9 cents to $33.18. Hiring highlights include +72k Leisure and Hospitality, +65k Education and Health Services, +47 Government, and +39k Professional and Business Services.

Job Openings & Labor Turnover Survey JOLTS – Released 4/4/2023 – The number of job openings decreased to 9.9 million on the last business day of February, the U.S. Bureau of Labor Statistics reported. Over the month, the number of hires and total separations changed little at 6.2 million and 5.8 million, respectively. Within separations, quits (4.0 million) increased, and layoffs and discharges (1.5 million) decreased.

Employment Cost Index – Released 1/31/2023 – Compensation costs for civilian workers increased 1.0% for the 3-month period ending in December 2022. The 12-month period ending on December 2022 saw compensation costs increase by 5.1%. The 12-month period ending December 2021 increased 4.0%. Wages and salaries increased 5.1 percent over the year and increased 4.5 percent for the 12-month period ending in December 2021. Benefit costs increased 4.9 percent over the year and increased 2.8 percent for the 12-month period ending in December 2021. This report is published quarterly.

This Week’s Economic Data

Links take you to the data source

Existing Home Sales – Released 4/20/2023 – Existing home sales decreased in March. Sales decreased 2.4% to a seasonally adjusted rate of 4.44 million in March. Sales decreased 22.0% year-over-year. Housing inventory sits at 980k units. Up 1.0% over February. Up 5.4% over last year. Unsold inventory sits at a 2.6-month supply. The median existing home price for all housing types was $375,700 which is down 0.9% from March 2022.

Housing Starts – Released 4/18/2023 – New home starts in March were at a seasonally adjusted annual rate of 1.420 million; down 0.8% below February, and 17.2% below last March’s rate. Building Permits were at a seasonally adjusted annual rate of 1.413 million, down 8.8% compared to February, and down 24.8% over last year.

Recent Economic Date

Links take you to the data source

Existing Home Sales – Released 4/20/2023 – Existing home sales decreased in March. Sales decreased 2.4% to a seasonally adjusted rate of 4.44 million in March. Sales decreased 22.0% year-over-year. Housing inventory sits at 980k units. Up 1.0% over February. Up 5.4% over last year. Unsold inventory sits at a 2.6-month supply. The median existing home price for all housing types was $375,700 which is down 0.9% from March 2022.

Housing Starts – Released 4/18/2023 – New home starts in March were at a seasonally adjusted annual rate of 1.420 million; down 0.8% below February, and 17.2% below last March’s rate. Building Permits were at a seasonally adjusted annual rate of 1.413 million, down 8.8% compared to February, and down 24.8% over last year.

Industrial Production and Capacity Utilization – Released 4/14/2023 – In March, Industrial production increased 0.4%. Manufacturing decreased 0.5%. Utilities output increased 8.4%. Mining output declined 0.5%. Total industrial production was 0.5% higher in March than a year ago. Total capacity utilization increased in March to 79.8% which is 0.1% above its long run average.

Retail Sales – Released 4/14/2023 – U.S. retail sales for March decreased 1.0% to $691.7 billion but retail sales are 2.9% above March 2022. U.S. retail sales for the January 2022 through March 2023 period were up 5.4% from the same period a year ago.

Producer Price Index – Released 4/13/2023 – The PPI for final demand decreased 0.5 percent in March, seasonally adjusted, the U.S. Bureau of Labor Statistics reported. Final demand prices were unchanged in February and increased 0.4 percent in January. On an unadjusted basis, the index for final demand increased 2.7 percent year over year.

Consumer Price Index – Released 4/12/2023 – Consumer prices increased 0.1% m/m in March following a 0.4% increase in February. Consumer prices are up 5.0% for the 12-month period ending in March. Core consumer prices increased 0.4% m/m in March.

Consumer Credit – Released 4/7/2023 – In February, consumer credit increased at a seasonally adjusted annual rate of 3.8 percent. Revolving credit increased at an annual rate of 5.0 percent, while nonrevolving credit increased at an annual rate of 3.4 percent.

U.S. Trade Balance – Released 4/5/2023 – The U.S. monthly international trade deficit increased in February 2023 according to the U.S. Bureau of Economic Analysis and the U.S. Census Bureau. The deficit increased from $68.7 billion in January (revised) to $70.5 billion in February. February exports were $251.2 billion, $6.9 billion less than January exports. February imports were $321.7 billion, $5.0 billion less than January imports. Year-to-date, the goods and services deficit decreased $35.5 billion, or 20.3 percent, from the same period in 2022. Exports increased $49.5 billion or 10.8 percent. Imports increased $14.0 billion or 2.2 percent.

PMI Non-Manufacturing Index – Released 4/5/2023 – Economic activity remained in expansionary territory in March. The Services PMI® registered 51.2 percent, 3.9 percentage points lower than February. In February, the Services PMI® registered 55.1 percent.

PMI Manufacturing Index – Released 4/3/2023 – The March Manufacturing PMI® registered 46.3 percent, 1.4 percentage point lower than the 47.7 percent recorded in February. Regarding the overall economy, this figure indicates four months of contraction following 30 months of expansion. The New Orders Index remained in contraction territory at 44.3 percent, 2.7 percentage points lower than the 47.0 percent recorded in February. The production index increased 0.5 percentage points to 47.8.

U.S. Construction Spending – Released 4/3/2023 – Construction spending during February 2023 was estimated at a seasonally adjusted annual rate of $1,844.4 billion, 0.1 percent below the revised January estimate of $1,845.4 billion. The February figure is 5.2 percent above the February 2022 estimate of $1,753.1 billion.

Data Sources:

Bureau of Economic Analysis (BEA)

Congressional Budget Office (CBO)

U.S. Bureau of Labor Statistics (BLS)

Federal Reserve Economic Data (FRED Charts)

CME Fed Watch

U.S. Treasury – Yields

U.S. Census Bureau

Institute for Supply Management (ISM)

Weekly DOL Employment Data

BLS Monthly Jobs Report

JOLTS

US Energy Admin (EIA)

BLS Consumer Price Index CPI

BLS Producer Price Index PPI

Atlanta Fed GDPNOW

NY Fed Nowcast GDP

US Census Bureau Housing Starts

Consumer Credit

USCB Retail Sales

Construction Spending

Federal Reserve Dot Plots

NY Empire Index

Philadelphia Federal Reserve

P/E Ratio Data -Yardeni Research

Technical Analysis Info:

StockCharts.com – Financial Charts

Exponential vs Simple moving average

Other Links:

1973 Arab Oil Embargo

Hunt Brothers Silver

Long-Term Capital bailout

Categories:

Tags: