Good Life Advisors – Talking Points – Week 27

PUBLISHED JULY 18, 2022.

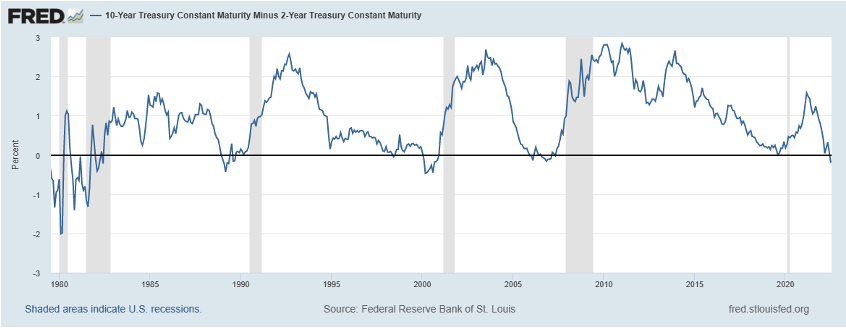

Two recession indicators are battling it out. The 10-year minus 2-year yield ended this week squarely in the “recession coming” area at a negative 20 bps. While the 10-year minus Fed funds isn’t even close to being negative at 138 bps.

Stocks finished the week modestly lower, though off the worst midweek levels that followed the hotter-than-expected June CPI print. Sectors were mostly lower and fairly mixed. Growth (-1.3%) was an underperformer to value (-0.9%) this week after last week’s 400 bp+ outperformance. Banks were mixed, with money centers modestly higher after the start of earnings season, outperforming smaller cap banks and regionals. Some of the worst performers included precious metals miners, commodity chemicals biotech, parcels and logistics, insurance, FANMAGs, and retail. Some of the gainers included airlines, semis, homebuilders, restaurants, and hotels. Treasuries were mostly firmer with curve flattening, with the 2Y/10Y inverting to the most since 2000. The dollar index was up 1%, higher for a third-straight week. The dollar saw solid gains on the major crosses, particularly the yen, while hitting parity with the euro for the first time this week in 20 years. Gold finished the week down 2.2%. WTI crude was down 6.9% and finishing back below $100 a barrel.

Wednesday’s June headline CPI was up 0.3pp to 1.3% m/m, above consensus for a 1.1% increase. Annualized CPI up 0.5pp to 9.1%, also above consensus 8.8% and highest since 1981. The hot print led to market to price in a 90% chance of a 100 bp hike at the July FOMC meeting. However, the odds of a 100 bp hike came off late in the week, falling below 30% on Friday, after Fed Governor Waller said a 75 bp rate hike is his base case for July. St. Louis’ Bullard (voter) also played down a 100 bp hike. However, Bullard said on Friday that the Fed needs to be more aggressive in 2H, and would like to see rates go up to 3.75-4%, above his previous 3.5% forecast. In the end, it’s simply a question of how much rates rise, not if.

Despite this week’s CPI report, there was more hope that inflation may be peaking. This week’s Michigan Consumer Sentiment report showed 5Y inflation expectations down 0.3pp to 2.8%, the lowest in a year. Gasoline prices also fell to four-week lows ($4.59 in our area now) with the demand destruction dynamic in focus after the DOE weekly showed gasoline demand down by 1.35M bpd, or more than 10%, in recent weeks. Commodities continued their recent selloff, with copper falling to a 20-month low, down 35% from the record prices of four months ago. Friday’s June retail sales report beat estimates, while retail sales ex-autos posted the fastest growth since March. There were questions into the print on what the market impact of a beat after Fed Governor Waller called out the report specifically as something that could favor a larger July rate hike. However, the bond market seemed to have been more focused on the reprieve around inflation concerns rather than hotter consumer spending trends.

S&P 500 earnings are expected to grow 4.1% y/y in Q2, which according to FactSet would represent the smallest expansion since Q4 2020. BofA analysts also warned this week that equity markets could see proper capitulation if Q2 earnings come in worse than expected. There have also been brad concerns that consensus EPS estimates need the be revised down to reflect the growth hit from tightening financial conditions, along with still elevated input price pressures and FX, putting guidance in focus. At the same time, the bar for Q2 may have been sufficiently lowered in recent weeks, a trend that has been reflected by some of the “better-than-feared” takeaways surrounding some of this week’s reporters, a theme Deutsche Bank touched on in its earnings preview (Bloomberg). Banks also rallied despite some weaker metrics on the surface, with some pointing to lowered expectations into this week’s prints.

Multiple strategists cut S&P price targets. BofA strategist Savita Subramanian cut her year-end S&P target to 3,600 from 4,500, or a 25% deadline. Subramanian also noted that the S&P could fall to 3,00-3,200 in a recession scenario. The update was based on lower EPS growth forecast for 2022 of +4% from +6%, while 2023 was cut from +6% to -8%, or a 10% peak to trough EPS decline. Subramanian also cited a higher equity risk premium given the Fed’s rate hikes into an overvalued, long duration market. UBS strategist Keith Parker also cut his S&P price target this week to 4,150, seeing modest upside given slowing growth but no recession, as well as decelerating inflation. Piper Sandler’s Michael Kantrowitz cut his year-end target to 3,400 from 4,00, or a ~11% decline in 2H, arguing that earnings expectations to weaken alongside economic slowdown.

Next week brings a number of key economic data reports ahead of the July 26-27 FOMC meeting. A big week of housing data include Monday’s July NAHB builder confidence, Tuesday’s June housing starts and building permits, and Wednesday’s existing home sales. Friday also brings Markit July flash PMIs, which are expected to reveal some sequential softening after manufacturing new orders fell into contraction last month and high frequency data continues to point to some leveling off in services following earlier normalization momentum.

Equities

Fixed Income

Yield Curve

June FOMC Statement Balance Sheet Reduction Plan Credit, Liquidity and Balance Sheet Federal Reserve Dot Plots

US Corporate Debt Tops 7 Trillion. Treasury.gov yields FOMC Policy Normalization Statement Longer Run Goals August 2020

Foreign Exchange Market

Europe travel looks really good these days as the USD/ Eur is almost level.

Energy Complex

The Baker Hughes rig count decreased by 4 this week. There are 756 oil and gas rigs operating in the US – Up 272 over last year.

Metals Complex

Employment Picture

Weekly Unemployment Claims – Released Thursday 7/14/2022 – The week ending July 9th observed an increased of 9k in initial claims increasing to 244k. The four-week moving average of initial jobless claims increased 3.25k to 235.75k.

June Jobs Report – BLS Summary – Released 7/8/2022 – The US Economy added 372k nonfarm jobs in June and the Unemployment rate stayed unchanged at 3.6%. Average hourly earnings increased 10 to $32.08. Hiring highlights include +67k Leisure and Hospitality, +96k Education and Health Services, and +74 Professional and Business Services.

- Average hourly earnings increased 10 cents to $32.08.

- U3 unemployment rate remained unchanged at 3.6%. U6 unemployment rate declined from 7.1% to 6.7%.

- The labor force participation rate was little changed at 62.2%.

- Average work week was unchanged at 34.5 hours.

Job Openings & Labor Turnover Survey – JOLTS – Released 7/6/2022 – The US Bureau of Labor Statistics reported the number and rate of job openings decreased to 11.3 million on the last business day of May. Over the month, hires were little changed at 6.5 million and separations were little changed at 6 million. Within separations, quits were little changed at 4.3 million. The layoffs and discharges rates were little changed at 1.4 million.

Employment Cost Index – Released 4/29/2022 – Compensation costs for civilian workers increased 1.4% for the 3-month period ending in March 2022. The 12-month period ending in March 2022 saw compensation costs increased by 4.5%. The 12-month period ending March 2021 increased 2.6%. Wages and salaries increased 4.7% over the year and increased 2.7% for the 12-month period ending in March 2021. Benefit costs increased 4.1% over the year and increased 2.5% for the 12-month period ending in March 2021. The report is published quarterly.

This Week’s Economic Data

Links take you to the data source

Industrial Production and Capacity Utilization – Released 7/15/2022 – In June, Industrial Production decreased 0.2%. Manufacturing decreased 0.5%. Utilities output decreased 1.4%. Mining output increased 1.7%. Total industrial production was 4.2% higher in June than a year ago. Total capacity utilization increased to 80% in June which is 0.4% below its long run average.

Retail Sales – Released 7/15/2022 – US retail sales for June increased 1% to $680.6 billion and retail sales are 8.4% above June 2021. US retail sales for the April 2022 through June 2022 period were up 8.1% from the same period a year ago.

Producer Price Index – Released 7/14/2022 – The Producer Price Index for final demand increased 1.1% in June. PPI less food and energy increased 0.5%. The change in PPI for final demand has increased 11.3% year/y.

Consumer Price Index – Released 7/13/2022 – Consumer prices rose 1.3% m/m in June following a 1% increased in May. Consumer prices are up 9.1% for the 12-month period ending in June. Core consumer prices increased 0.7% m/m in June.

Recent Economic Data

Links take you to the data source

Consumer Credit – Released 7/8/2022 – Consumer credit increased at a seasonally adjusted annual rate of 5.9% in May. Revolving credit increased at an annual rate of 8.1%, while nonrevolving credit increased at an annual rate of 5.2%.

U.S. Trade Balance – Released 7/7/2022 – According to the US Census Bureau of Economic Analysis the goods and services deficit decreased in May by $1.1 billion to $85.5 billion. May exports were $255.9 billion, $3 billion more than April exports. May imports were $341.4 billion, $1.9 billion more than April imports. Year to date, the goods and services deficit increased $126.5 billion, or 38.4%, from the same period in 2021. Exports increased $197.1 billion or 19.4%. Imports increased $323.6 billion or 24%.

PMI Non-Manufacturing Index – Released 7/6/2022 – Economic activity in the non-manufacturing sector grew in June for the 25th consecutive month. ISM Non-Manufacturing registered 55.3%, which is 0.6 percentage points below the May reading of 55.9%.

PMI Manufacturing Index – Released 7/1/2022 – June PMI decreased 3.1% to 53% down from May’s reading of 56.1%. The New Orders Index was 49.2% down 5.9% from May’s reading of 55.1%. The Production Index registered 54.9%, up 0.7%.

U.S. Construction Spending – Released 7/1/2022 – Construction spending increased 0.1% in May measuring at a seasonally adjusted annual rate of $1,779.8 billion. The May figure is 9.7% above the May 2021 estimate. Private construction spending was unchanged from the revised April estimate at $1,436 billion. Public construction spending was 0.8% below the revised April estimate at $343.8 billion.

US Light Vehicle Sales – Released 6/30/2022 – US light vehicle sales were at a seasonally adjusted annual rate of 12.676 million units in May.

Chicago PMI – Released 6/30/2022 – Chicago PMI decreased by 4.3 points in June to 56. All five of the main five indications increased except for supplier deliveries, which hit its lowest level since November 2020.

Personal Income – Released 6/30/2022 – Personal income increased $113.4 billion or 0.5% in May according to estimates released today by the Bureau of Economic Analysis. Disposable Personal Income (DPI) increased $96.5 billion or 0.5% and Personal Consumption Expenditures (PCE) increased $32.7 billion or 0.2%.

Third Estimate of 1st Quarter 2022 GDP – Released 6/29/2022 – Real Gross Domestic Product (GDP) decreased at an annual rate of 1.6% in the first quarter of 2022, according to the third estimate released by the Bureau of Economic Analysis. GDP increased 6.9% in the fourth quarter of 2021. The GDP third estimate is based on data that are more complete than the advance estimate which estimated that GDP declined 1.4% in the first quarter and then the second estimate which estimated that GDP declined 1.5% in the first quarter. The third estimate primarily reflects a downward revision to Personal Consumption Expenditures (PCE) that was partly offset by an upward revision to private inventory investment. The decrease in real GDP reflected decreases in private inventory investment, exports, federal government spending, and state and local government spending, while imports, which are a subtraction in the calculation of GDP, increased. Personal Consumption Expenditures (PCE), nonresidential fixed investment, and residential fixed investment increased.

Consumer Confidence – Released 6/28/2022 – The consumer confidence index decreased in June following a decline in May. The Index now stands at 98.7, down from 103.2 in May.

Durable Goods – Released 6/27/2022 – New orders for manufactured durable goods in May increased $1.9 billion or 0.7% to $267.2 billion. Transportation equipment led the increase up $0.7 billion or 0.8% to $87.6 billion.

New Residential Sales – Released 6/24/2022 – Sales of new single-family homes increased 10.7% to 696k, seasonally adjusted, in May. The median sales price of new homes sold in May was $449,000 with an average sales price of $511,400/ At the end of May, the seasonally adjusted estimate of new homes for sale was 444k. This represents a supply of 7.7 months at the current sales rate.

Existing Home Sales – Released 6/21/2022 – Existing home sales decreased in May marking four consecutive months of declines. Sales declined 3.4% to a seasonally adjusted rate of 5.61 million in Mat. Sales decreased 8.6% year-over-year. Housing inventory sits at 1.16 million units. Up 12.6% from April’s inventory. Down 4.1% over last year. Unsold inventory sits at a 2.6-month supply. The median existing home price for all housing types was $407,600 which is up 14.8% from May 2021. This marks 123 consecutive months of year-over-year increases, the longest-running streak on record.

Housing Starts – Released 6/16/2022 – New home starts on May were at a seasonally adjusted annual rate of 1.549 million; down 14.4% below April, and 3.5% below last May’s rate. Building Permits were at a seasonally adjusted annual rate of 1.695 million, down 7% compared to April, but up 0.2% over last year.

Next week we get data on Existing Home Sales and Housing Starts.

Data Sources:

Bureau of Economic Analysis (BEA)

Congressional Budget Office (CBO)

U.S. Bureau of Labor Statistics (BLS)

Federal Reserve Economic Data (FRED Charts)

CME Fed Watch

U.S. Treasury – Yields

U.S. Census Bureau

Institute for Supply Management (ISM)

Weekly DOL Employment Data

BLS Monthly Jobs Report

JOLTS

US Energy Admin (EIA)

BLS Consumer Price Index CPI

BLS Producer Price Index PPI

Atlanta Fed GDPNOW

NY Fed Nowcast GDP

US Census Bureau Housing Starts

Consumer Credit

USCB Retail Sales

Construction Spending

Federal Reserve Dot Plots

NY Empire Index

Philadelphia Federal Reserve

P/E Ratio Data -Yardeni Research

Technical Analysis Info:

StockCharts.com – Financial Charts

Exponential vs Simple moving average

Other Links:

1973 Arab Oil Embargo

Hunt Brothers Silver

Long-Term Capital bailout

Week 27 Talking Points

Good Life Advisors – Talking Points – Week 27

PUBLISHED JULY 18, 2022.

Two recession indicators are battling it out. The 10-year minus 2-year yield ended this week squarely in the “recession coming” area at a negative 20 bps. While the 10-year minus Fed funds isn’t even close to being negative at 138 bps.

Stocks finished the week modestly lower, though off the worst midweek levels that followed the hotter-than-expected June CPI print. Sectors were mostly lower and fairly mixed. Growth (-1.3%) was an underperformer to value (-0.9%) this week after last week’s 400 bp+ outperformance. Banks were mixed, with money centers modestly higher after the start of earnings season, outperforming smaller cap banks and regionals. Some of the worst performers included precious metals miners, commodity chemicals biotech, parcels and logistics, insurance, FANMAGs, and retail. Some of the gainers included airlines, semis, homebuilders, restaurants, and hotels. Treasuries were mostly firmer with curve flattening, with the 2Y/10Y inverting to the most since 2000. The dollar index was up 1%, higher for a third-straight week. The dollar saw solid gains on the major crosses, particularly the yen, while hitting parity with the euro for the first time this week in 20 years. Gold finished the week down 2.2%. WTI crude was down 6.9% and finishing back below $100 a barrel.

Wednesday’s June headline CPI was up 0.3pp to 1.3% m/m, above consensus for a 1.1% increase. Annualized CPI up 0.5pp to 9.1%, also above consensus 8.8% and highest since 1981. The hot print led to market to price in a 90% chance of a 100 bp hike at the July FOMC meeting. However, the odds of a 100 bp hike came off late in the week, falling below 30% on Friday, after Fed Governor Waller said a 75 bp rate hike is his base case for July. St. Louis’ Bullard (voter) also played down a 100 bp hike. However, Bullard said on Friday that the Fed needs to be more aggressive in 2H, and would like to see rates go up to 3.75-4%, above his previous 3.5% forecast. In the end, it’s simply a question of how much rates rise, not if.

Despite this week’s CPI report, there was more hope that inflation may be peaking. This week’s Michigan Consumer Sentiment report showed 5Y inflation expectations down 0.3pp to 2.8%, the lowest in a year. Gasoline prices also fell to four-week lows ($4.59 in our area now) with the demand destruction dynamic in focus after the DOE weekly showed gasoline demand down by 1.35M bpd, or more than 10%, in recent weeks. Commodities continued their recent selloff, with copper falling to a 20-month low, down 35% from the record prices of four months ago. Friday’s June retail sales report beat estimates, while retail sales ex-autos posted the fastest growth since March. There were questions into the print on what the market impact of a beat after Fed Governor Waller called out the report specifically as something that could favor a larger July rate hike. However, the bond market seemed to have been more focused on the reprieve around inflation concerns rather than hotter consumer spending trends.

S&P 500 earnings are expected to grow 4.1% y/y in Q2, which according to FactSet would represent the smallest expansion since Q4 2020. BofA analysts also warned this week that equity markets could see proper capitulation if Q2 earnings come in worse than expected. There have also been brad concerns that consensus EPS estimates need the be revised down to reflect the growth hit from tightening financial conditions, along with still elevated input price pressures and FX, putting guidance in focus. At the same time, the bar for Q2 may have been sufficiently lowered in recent weeks, a trend that has been reflected by some of the “better-than-feared” takeaways surrounding some of this week’s reporters, a theme Deutsche Bank touched on in its earnings preview (Bloomberg). Banks also rallied despite some weaker metrics on the surface, with some pointing to lowered expectations into this week’s prints.

Multiple strategists cut S&P price targets. BofA strategist Savita Subramanian cut her year-end S&P target to 3,600 from 4,500, or a 25% deadline. Subramanian also noted that the S&P could fall to 3,00-3,200 in a recession scenario. The update was based on lower EPS growth forecast for 2022 of +4% from +6%, while 2023 was cut from +6% to -8%, or a 10% peak to trough EPS decline. Subramanian also cited a higher equity risk premium given the Fed’s rate hikes into an overvalued, long duration market. UBS strategist Keith Parker also cut his S&P price target this week to 4,150, seeing modest upside given slowing growth but no recession, as well as decelerating inflation. Piper Sandler’s Michael Kantrowitz cut his year-end target to 3,400 from 4,00, or a ~11% decline in 2H, arguing that earnings expectations to weaken alongside economic slowdown.

Next week brings a number of key economic data reports ahead of the July 26-27 FOMC meeting. A big week of housing data include Monday’s July NAHB builder confidence, Tuesday’s June housing starts and building permits, and Wednesday’s existing home sales. Friday also brings Markit July flash PMIs, which are expected to reveal some sequential softening after manufacturing new orders fell into contraction last month and high frequency data continues to point to some leveling off in services following earlier normalization momentum.

Table of Contents

Equities

Fixed Income

Yield Curve

June FOMC Statement Balance Sheet Reduction Plan Credit, Liquidity and Balance Sheet Federal Reserve Dot Plots

US Corporate Debt Tops 7 Trillion. Treasury.gov yields FOMC Policy Normalization Statement Longer Run Goals August 2020

Foreign Exchange Market

Europe travel looks really good these days as the USD/ Eur is almost level.

Energy Complex

The Baker Hughes rig count decreased by 4 this week. There are 756 oil and gas rigs operating in the US – Up 272 over last year.

Metals Complex

Employment Picture

Weekly Unemployment Claims – Released Thursday 7/14/2022 – The week ending July 9th observed an increased of 9k in initial claims increasing to 244k. The four-week moving average of initial jobless claims increased 3.25k to 235.75k.

June Jobs Report – BLS Summary – Released 7/8/2022 – The US Economy added 372k nonfarm jobs in June and the Unemployment rate stayed unchanged at 3.6%. Average hourly earnings increased 10 to $32.08. Hiring highlights include +67k Leisure and Hospitality, +96k Education and Health Services, and +74 Professional and Business Services.

Job Openings & Labor Turnover Survey – JOLTS – Released 7/6/2022 – The US Bureau of Labor Statistics reported the number and rate of job openings decreased to 11.3 million on the last business day of May. Over the month, hires were little changed at 6.5 million and separations were little changed at 6 million. Within separations, quits were little changed at 4.3 million. The layoffs and discharges rates were little changed at 1.4 million.

Employment Cost Index – Released 4/29/2022 – Compensation costs for civilian workers increased 1.4% for the 3-month period ending in March 2022. The 12-month period ending in March 2022 saw compensation costs increased by 4.5%. The 12-month period ending March 2021 increased 2.6%. Wages and salaries increased 4.7% over the year and increased 2.7% for the 12-month period ending in March 2021. Benefit costs increased 4.1% over the year and increased 2.5% for the 12-month period ending in March 2021. The report is published quarterly.

This Week’s Economic Data

Links take you to the data source

Industrial Production and Capacity Utilization – Released 7/15/2022 – In June, Industrial Production decreased 0.2%. Manufacturing decreased 0.5%. Utilities output decreased 1.4%. Mining output increased 1.7%. Total industrial production was 4.2% higher in June than a year ago. Total capacity utilization increased to 80% in June which is 0.4% below its long run average.

Retail Sales – Released 7/15/2022 – US retail sales for June increased 1% to $680.6 billion and retail sales are 8.4% above June 2021. US retail sales for the April 2022 through June 2022 period were up 8.1% from the same period a year ago.

Producer Price Index – Released 7/14/2022 – The Producer Price Index for final demand increased 1.1% in June. PPI less food and energy increased 0.5%. The change in PPI for final demand has increased 11.3% year/y.

Consumer Price Index – Released 7/13/2022 – Consumer prices rose 1.3% m/m in June following a 1% increased in May. Consumer prices are up 9.1% for the 12-month period ending in June. Core consumer prices increased 0.7% m/m in June.

Recent Economic Data

Links take you to the data source

Consumer Credit – Released 7/8/2022 – Consumer credit increased at a seasonally adjusted annual rate of 5.9% in May. Revolving credit increased at an annual rate of 8.1%, while nonrevolving credit increased at an annual rate of 5.2%.

U.S. Trade Balance – Released 7/7/2022 – According to the US Census Bureau of Economic Analysis the goods and services deficit decreased in May by $1.1 billion to $85.5 billion. May exports were $255.9 billion, $3 billion more than April exports. May imports were $341.4 billion, $1.9 billion more than April imports. Year to date, the goods and services deficit increased $126.5 billion, or 38.4%, from the same period in 2021. Exports increased $197.1 billion or 19.4%. Imports increased $323.6 billion or 24%.

PMI Non-Manufacturing Index – Released 7/6/2022 – Economic activity in the non-manufacturing sector grew in June for the 25th consecutive month. ISM Non-Manufacturing registered 55.3%, which is 0.6 percentage points below the May reading of 55.9%.

PMI Manufacturing Index – Released 7/1/2022 – June PMI decreased 3.1% to 53% down from May’s reading of 56.1%. The New Orders Index was 49.2% down 5.9% from May’s reading of 55.1%. The Production Index registered 54.9%, up 0.7%.

U.S. Construction Spending – Released 7/1/2022 – Construction spending increased 0.1% in May measuring at a seasonally adjusted annual rate of $1,779.8 billion. The May figure is 9.7% above the May 2021 estimate. Private construction spending was unchanged from the revised April estimate at $1,436 billion. Public construction spending was 0.8% below the revised April estimate at $343.8 billion.

US Light Vehicle Sales – Released 6/30/2022 – US light vehicle sales were at a seasonally adjusted annual rate of 12.676 million units in May.

Chicago PMI – Released 6/30/2022 – Chicago PMI decreased by 4.3 points in June to 56. All five of the main five indications increased except for supplier deliveries, which hit its lowest level since November 2020.

Personal Income – Released 6/30/2022 – Personal income increased $113.4 billion or 0.5% in May according to estimates released today by the Bureau of Economic Analysis. Disposable Personal Income (DPI) increased $96.5 billion or 0.5% and Personal Consumption Expenditures (PCE) increased $32.7 billion or 0.2%.

Third Estimate of 1st Quarter 2022 GDP – Released 6/29/2022 – Real Gross Domestic Product (GDP) decreased at an annual rate of 1.6% in the first quarter of 2022, according to the third estimate released by the Bureau of Economic Analysis. GDP increased 6.9% in the fourth quarter of 2021. The GDP third estimate is based on data that are more complete than the advance estimate which estimated that GDP declined 1.4% in the first quarter and then the second estimate which estimated that GDP declined 1.5% in the first quarter. The third estimate primarily reflects a downward revision to Personal Consumption Expenditures (PCE) that was partly offset by an upward revision to private inventory investment. The decrease in real GDP reflected decreases in private inventory investment, exports, federal government spending, and state and local government spending, while imports, which are a subtraction in the calculation of GDP, increased. Personal Consumption Expenditures (PCE), nonresidential fixed investment, and residential fixed investment increased.

Consumer Confidence – Released 6/28/2022 – The consumer confidence index decreased in June following a decline in May. The Index now stands at 98.7, down from 103.2 in May.

Durable Goods – Released 6/27/2022 – New orders for manufactured durable goods in May increased $1.9 billion or 0.7% to $267.2 billion. Transportation equipment led the increase up $0.7 billion or 0.8% to $87.6 billion.

New Residential Sales – Released 6/24/2022 – Sales of new single-family homes increased 10.7% to 696k, seasonally adjusted, in May. The median sales price of new homes sold in May was $449,000 with an average sales price of $511,400/ At the end of May, the seasonally adjusted estimate of new homes for sale was 444k. This represents a supply of 7.7 months at the current sales rate.

Existing Home Sales – Released 6/21/2022 – Existing home sales decreased in May marking four consecutive months of declines. Sales declined 3.4% to a seasonally adjusted rate of 5.61 million in Mat. Sales decreased 8.6% year-over-year. Housing inventory sits at 1.16 million units. Up 12.6% from April’s inventory. Down 4.1% over last year. Unsold inventory sits at a 2.6-month supply. The median existing home price for all housing types was $407,600 which is up 14.8% from May 2021. This marks 123 consecutive months of year-over-year increases, the longest-running streak on record.

Housing Starts – Released 6/16/2022 – New home starts on May were at a seasonally adjusted annual rate of 1.549 million; down 14.4% below April, and 3.5% below last May’s rate. Building Permits were at a seasonally adjusted annual rate of 1.695 million, down 7% compared to April, but up 0.2% over last year.

Next week we get data on Existing Home Sales and Housing Starts.

Data Sources:

Bureau of Economic Analysis (BEA)

Congressional Budget Office (CBO)

U.S. Bureau of Labor Statistics (BLS)

Federal Reserve Economic Data (FRED Charts)

CME Fed Watch

U.S. Treasury – Yields

U.S. Census Bureau

Institute for Supply Management (ISM)

Weekly DOL Employment Data

BLS Monthly Jobs Report

JOLTS

US Energy Admin (EIA)

BLS Consumer Price Index CPI

BLS Producer Price Index PPI

Atlanta Fed GDPNOW

NY Fed Nowcast GDP

US Census Bureau Housing Starts

Consumer Credit

USCB Retail Sales

Construction Spending

Federal Reserve Dot Plots

NY Empire Index

Philadelphia Federal Reserve

P/E Ratio Data -Yardeni Research

Technical Analysis Info:

StockCharts.com – Financial Charts

Exponential vs Simple moving average

Other Links:

1973 Arab Oil Embargo

Hunt Brothers Silver

Long-Term Capital bailout

Categories:

Tags: